The evolution of banking

Jun 20, 2024

From ancient banking branches to omnichannel digital services, the history of banking has been shaped by economics, innovation, and — of course — financial fraud

The way we bank has changed dramatically over centuries, then decades, then years. The evolution of banking has come about by shifts in wealth distribution, credit decisioning methods, client preferences, market structure, banking regulations, and technology.

Advancements like the introduction of credit cards, ATMs, online banking, mobile apps, and embedded finance have created new models for how banking customers access and manage their funds. Today, banking customers are increasingly empowered by real-time account access, budgeting tools, personalized financial insights, and more seamless digital customer journeys.

But when it comes to fraud, we often see a pattern where what is old eventually becomes new again. To prepare for successful banking experiences in the future, we first must know where we are coming from.

In this blog post, we'll explore the evolution of banking from the early days of in-branch banking to the rise of digital. We’ll also touch on how fraud prevention has changed amid widespread advancements, including the rise of omnichannel.

2000 BC — Religious temples safeguard assets for wealthy clients

The first banks began in consecrated temples around 2000 BC, many of which held money and treasure beneath them. Kings in ancient India, Syria, and Egypt would finance temples and later become patrons. Ancient temples conducted many of the same financial activities as modern banks, including deposit holding, lending, and wealth management.

Wealthy or royal clients felt comfortable with their assets in the hands of priests, who kept track of deposits and loans. Armed guards regularly patrolled temple grounds to prevent unauthorized parties from entering. At the time, early examples of fraud may have ranged from covert intrusion (via an early form of identity disguise) to employee theft and orchestrated temple ransacking by armed opposition groups.

In Rome, the ancient Temple of Saturn once housed the Roman Empire’s public treasury. The Temple of Juno Moneta acted as an extension of Roman minting facilities, storing coin-making supplies as of around 269 BC when silver coinage was first introduced to the empire. Minting supplies were removed from the temple by the end of the first century, as the Romans moved to formalize this and other banking operations in district buildings.

Some of the best-preserved temples still have bank-like reservoirs today. In 2011, Indian courts mandated an audit of the Anantha Padmanabhaswamy Temple’s underground vaults. The resulting audit revealed that the temple—first built around 5000 years ago—contains assets exceeding $20 billion. Unopened “Vault B” is estimated to contain assets worth at least one trillion dollars today.

The Anantha Padmanabhaswamy Temple is currently owned and operated by the Travancore Royal Family Trust, which possesses several properties, including other temples. While temples may not have scaled their banking operations for the modern world, the Indian government’s audit of the Anantha Padmanabhaswamy Temple alludes to the regulatory oversight of modern banking.

200 BC — Vendors exchange currency at Roman temples

Over time, ancient temples became sites of commerce, where vendors gathered to exchange goods. In Rome, the argentarii — a citizen’s guild of currency specialists — would convert foreign mints into Roman coins in exchange for a small fee at state-owned stalls around the Roman Forum. The argentarii were qualified to perform functions resembling modern-day banking, like making payments on behalf of others, lending, facilitating large payments (such as during auctions), deciding the value of coins, detecting forgeries, and circulating newly minted money. The argentarii even offered deposit options with and without interest.

Image Source: Smarthistory

The Roman state also appointed public bankers to assist the lower class, usually under special circumstances like periods of poverty during wartime. This role was developed to avert social unrest by helping citizens experiencing financial hardship overcome economic difficulties.

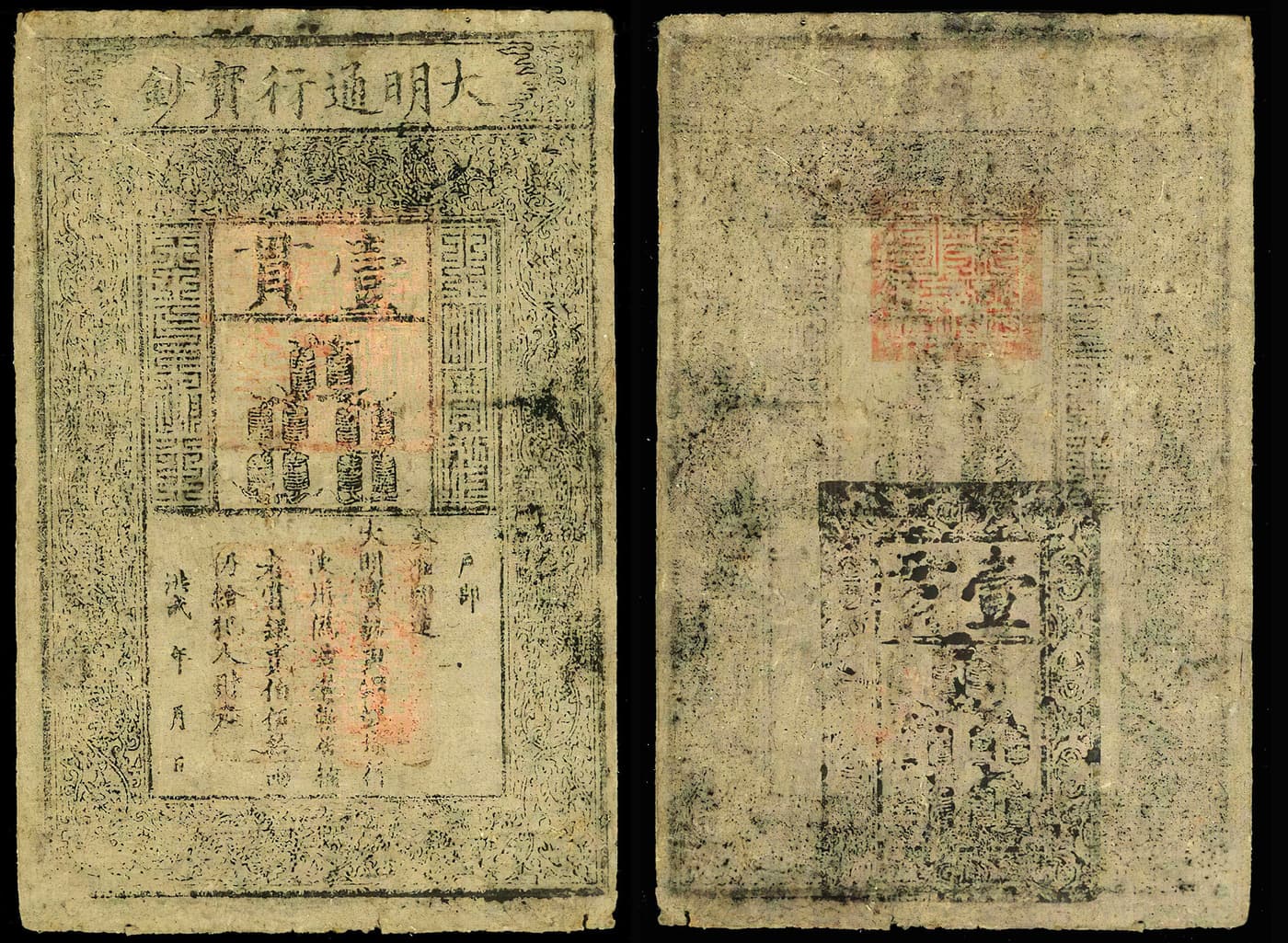

600 AD — China invents paper currency

From roughly 378 BCE onward, China used bronze or copper coins as its basic currency unit. These coins had holes in the center, which merchants would string to help them calculate or execute large transactions. The weight of these coins made them cumbersome to transport as commerce expanded and trading voyages grew.

Image Source: Coin Community

In the 7th century, Chinese merchants began using paper receipts of deposits to avoid carrying coinage long distances. During the Song dynasty, a small group of shops were granted the exclusive right to issue these certificates of deposit. In the 1020s, the government took control of the system, creating the world's first government-issued paper money.

Image Source: ADP

Leaders of the Mongol Yuan dynasty (1206-1367) eventually banned coinage altogether in a move that encouraged an all-paper economy. Marco Polo, the first Westerner to record the Chinese use of paper money, noted:

“All these pieces of paper are issued with as much solemnity and authority as if they were of pure gold or silver; and on every piece, a variety of officials, whose duty it is, have to write their names, and put their seals. And when all is prepared duly, the chief officer deputed by the Khan smears the seal entrusted to him with vermilion and impresses it on the paper, so that the form of the seal remains imprinted upon it in red; the money is then authentic. Anyone forging it would be punished with death.”

Paper money, backed by the state's authority, astonished Europe and reshaped the financial world. But paper banking didn’t stick right away: unfortunately, early fraud prevention systems like death threats weren’t enough to stop fraudsters. In a disastrous move for Chinese trade, the Ming dynasty discontinued paper money by 1455 to solve a counterfeit problem and reverse an overissuance of currency. It was only in the 19th century that paper money was reintegrated into China’s currency system.

1300s — Banking families grow branches in Italy

Long before today’s commercial banks, credit unions, and fintechs, banking families ruled Europe’s financial ecosystem. Between the 13th and 15th centuries, as coastal trade grew and the Catholic church lessened its grip on economic activity, Florentine family banks like the Medici, the Bardi, and the Peruzzi, brought major advancements to a budding global banking system.

Image Source: Museums of Florence

In medieval times, banks were run by merchant families that had amassed large amounts of wealth from trading goods like textiles. These families had the capital, space, security, and trust to house their city’s valuables. Local vendors, manufacturers, clergy, and nobility expected and needed these banking families to safeguard their assets from theft and fraud.

In Italy, the Medici branches worked closely together to offer clients early banking transfers and lines of credit as well as settle claims. To prevent fraud, the Medici Bank leveraged meticulous recordkeeping, identity verification processes, and transaction recalls. Authentication methods like seals, signatures, witnesses, and sometimes even coded messages helped bankers confirm the legitimacy of documents and detect forgery.

Even in medieval banking, some customer segments posed elevated risks. As Emmanuel N Roussakis explains in the academic article, Global Banking: Origins and Evolution, “Clergy and nobility were generally perceived as high risks, and credit was allowed only on a collateralized basis, e.g., the pledge of jewels and other personal assets, land, and revenues from mines, customs, or tax receipts. Credit limits were set for loans to other banks in Italy and for selected officials of the Church (e.g., cardinals and the Pope).” Like many banks today, the Medicis decided on credit and risk tolerance at their headquarters, aiming to apply these uniformly across their branches.

The Medici family’s risk tolerance was informed in part by a lending disaster that had left their predecessors bankrupt. In the 14th century, Edward III of England borrowed 1.5 million gold florins from two Italian families, the Bardis (900,000 florins) and the Peruzzis (600,000 florins), which he never repaid. This catastrophic example of a loan default led to the downfall of both the Bardi and Peruzzi family banks, the aftermath of which caused what some historians consider to be the worst financial collapse in history.

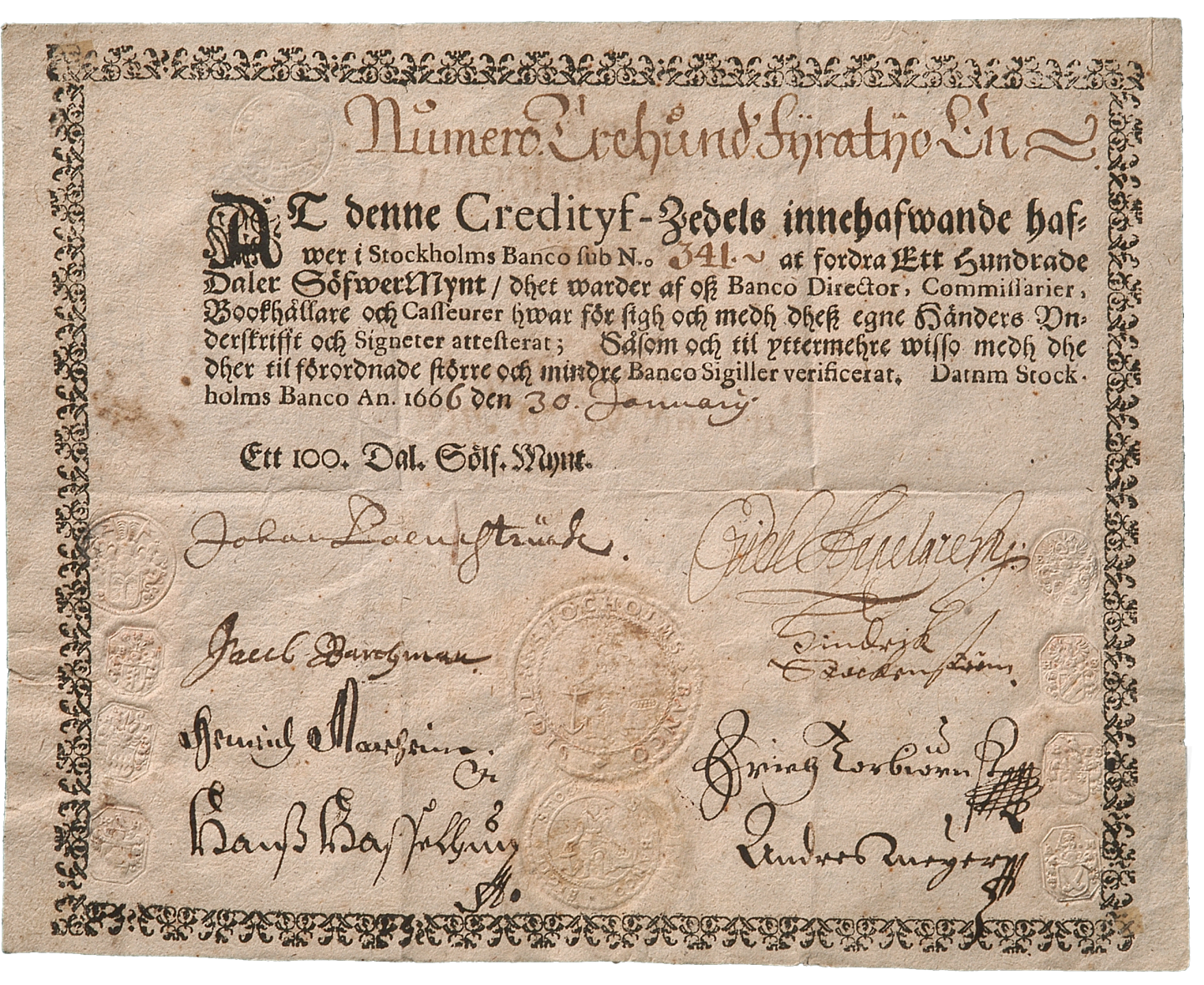

1600s — Europe issues its first banking notes

As trade increased, carrying and exchanging coinage became increasingly impractical. In the 14th and 15th centuries, European banks began releasing bills of exchange as a safer, more convenient alternative to coins. These bills, written from one bank to another in a different location, promised to pay a specific person a specified sum within a set timeframe. Much like the Chinese merchants before them, Europeans shifted away from coin transactions due to factors like transportation security, coin availability, and bulk.

The first European banking notes were issued in Sweden in 1661 by Johan Palmstruch, founder of Sweden's first bank, Stockholms Banco. The year prior, the Swedish government had begun minting new coins that were less heavy than previous iterations. Aware that their older, heavier coins had a higher material value, Stockholms Banco clients initiated a bank run.

Image Source: Riksbank

To counteract the bank run, Palmstruch offered his clients deposit certificates expressing their right to withdraw the deposited amount in coins. The banknotes had fixed denominations, no date limits, and were usable for general circulation. Despite Stockholms Banco’s eventual failure due to insufficient reserve funds, paper money continued to grow in popularity in Europe well into the 18th century, when banknote insurance was finally established.

1800s — Credit unions are born

The first credit unions were established in rural Germany in the 1850s and 1860s. Hermann Schulze-Delitzsch and Friedrich Wilhelm Raiffeisen created credit unions as a means of extending resources to farmers and workers who lacked access to traditional banking services. The purpose of credit unions was to promote self-governance, stability, community, and financial independence.

By pooling their savings and providing loans to one another, credit union members could overcome their dependency on banks while extending credit to their neighbors. This groundbreaking approach to community-based banking laid the foundation for modern credit unions worldwide.

1930s — Federal regulators insure bank deposits and authorize credit unions in the US

By the 1900s, the credit union movement had reached North America via Canada. As 20th-century financial options grew, new government bodies and laws also emerged to regulate bank and credit union activity.

In the United States, the Banking Act of 1933 gave way to the Federal Deposit Insurance Corporation (FDIC). If a bank failure were to occur, the FDIC provided greater security for depositors and borrowers by protecting insured deposits.

President Franklin Delano Roosevelt signed the Federal Credit Union Act in 1934, authorizing the formation of federally chartered credit unions in the US and establishing a federal bureau to oversee and regulate these institutions. Unfortunately, credit unions weren’t federally insured in the US until Congress created the National Credit Union Share Insurance Fund, almost 40 years after the FDIC was first introduced.

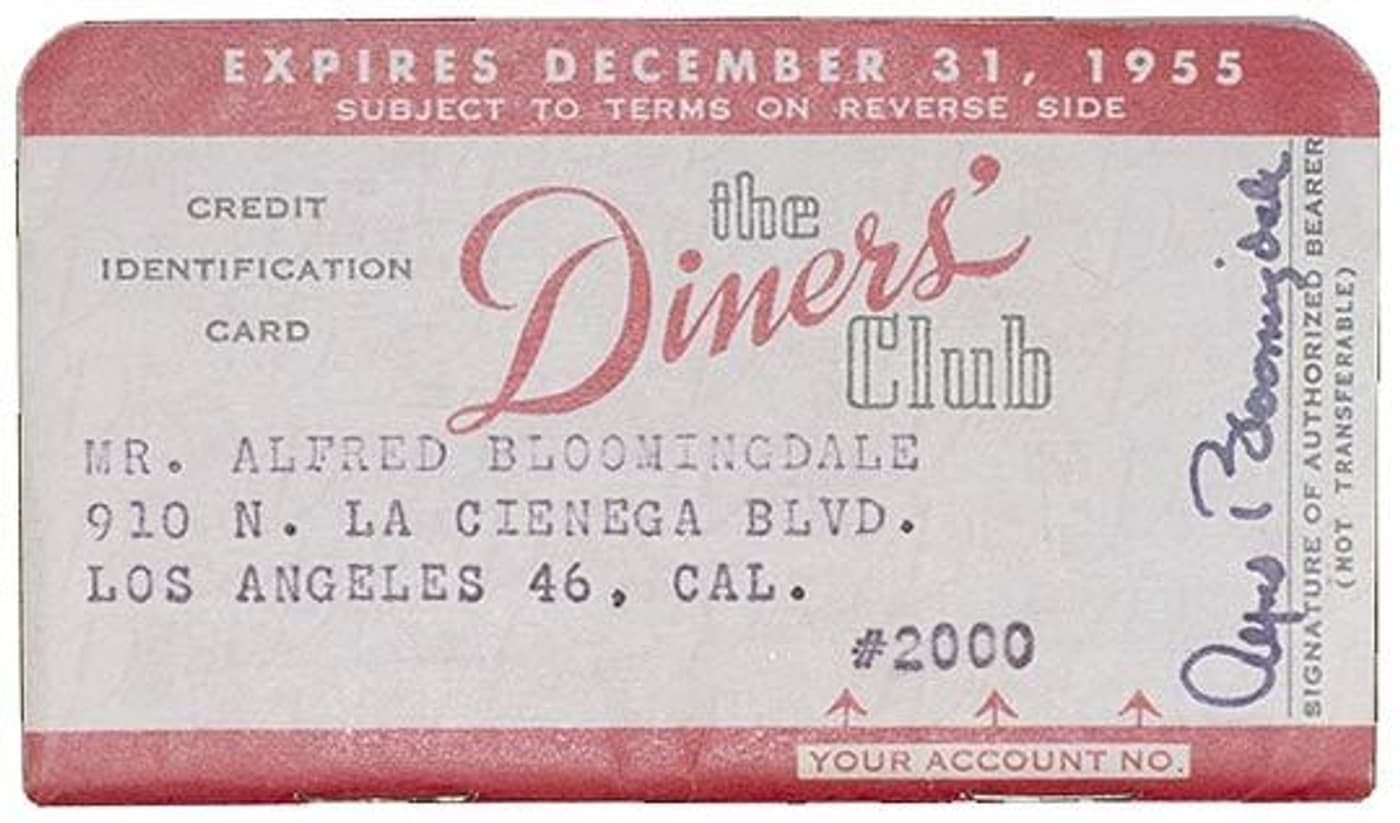

1950s — Credit cards gain traction

For centuries, merchants have allowed trusted customers to make purchases on credit and pay later. But the modern credit card as we know it today emerged in New York City in the 1950s, when the Diners Club introduced a cardboard card that allowed people to make purchases at participating restaurants and hotels without carrying cash. The convenience and flexibility offered by this novel payment method quickly gained popularity among affluent consumers and business travelers.

Image Source: Smithsonian

Other banks soon followed suit. In 1958, American Express launched its own plastic credit card, expanding the concept beyond dining and travel. The same year, Visa was founded when Bank of America introduced the BankAmericard (the card was later rebranded). It was the first credit card that could be used by a wide variety of merchants.

The BankAmericard was also one of the first credit cards to experience wide-scale fraud: In a trial marketing attempt, Bank of America randomly issued 60,000 activated credit cards to residents of Fresno, California, each preapproved for between $300 and $500. The project experienced crippling amounts of fraud, with 22% of payments reported delinquent in the program’s early days.

As Gabriel Dillard of The Business Journal explains, “the Bank of America executive who created the program, resigned his position about a year and a half after the Fresno Drop. With no experience in installment lending, he didn’t think to build up a collections or fraud department ahead of time. By the time he quit, the bank had lost $8.8 million on the program. The real figure — factoring in marketing and overhead — was closer to $20 million.”

Credit cards offered instant access to money, enabling people to make purchases they might not have been able to afford otherwise. This stimulated consumer spending and helped drive economic growth. But new challenges related to fraud and security also emerged. As stolen cards and unauthorized transactions became more common, new enhanced security features such as magnetic stripes and signatures were developed to help banks keep up with fraudsters.

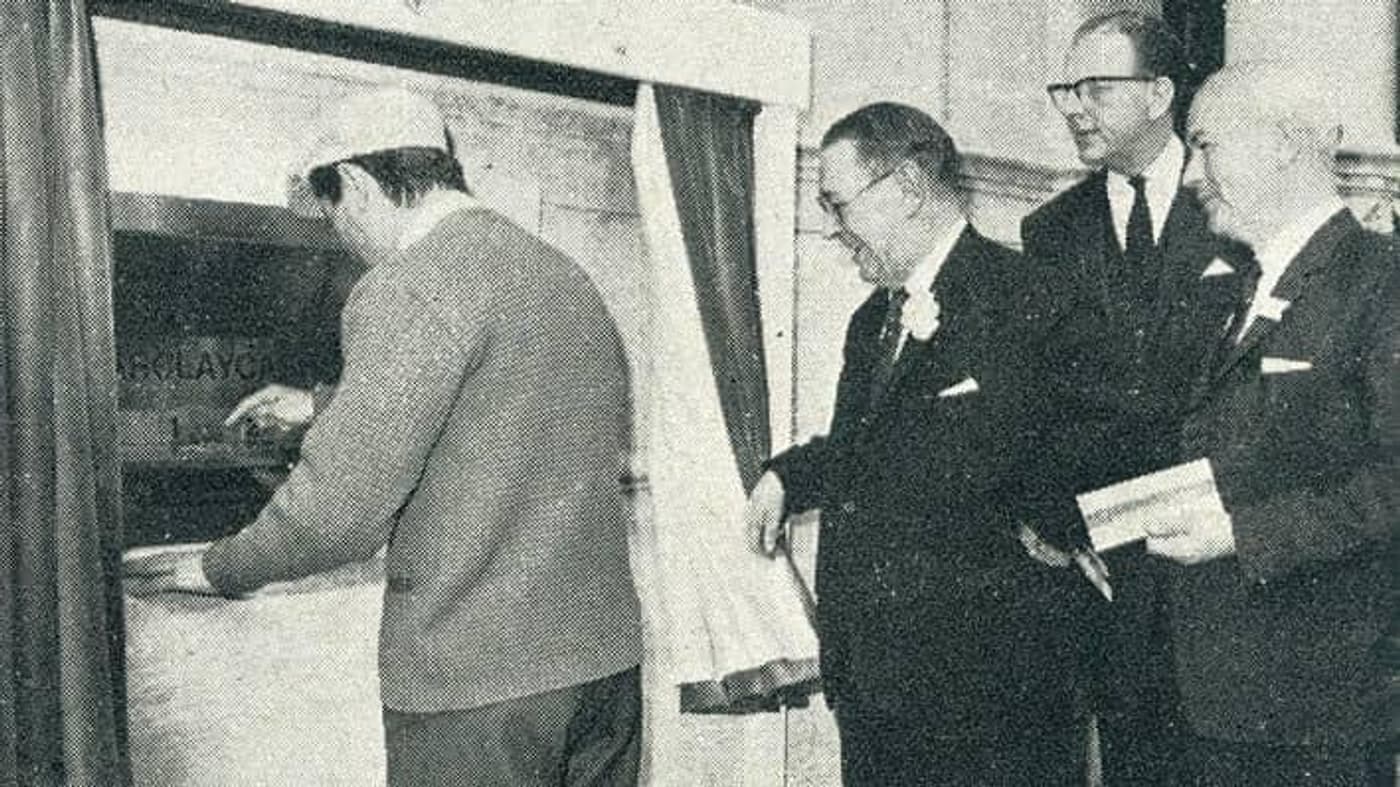

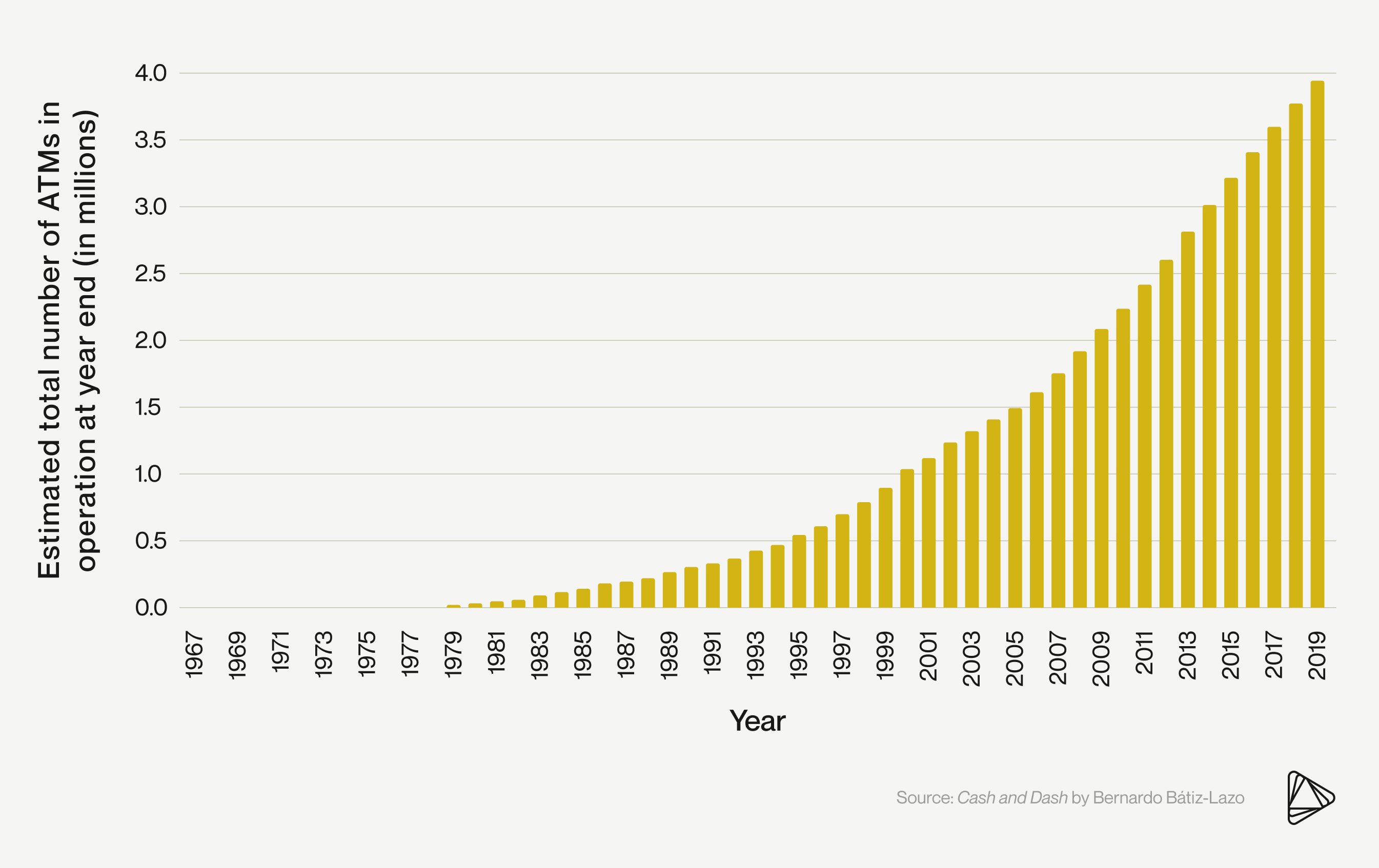

1960s — The first ATM withdrawal takes place in the UK

In a game-changing response to the demand for cash, Barclays deployed the first ATM in 1967 in the British suburb of Enfield. The bank chose British actor, Reg Varney, to be the first person to use the ATM. At the time, the machine only dispensed £1 notes, offering a total of £10 per withdrawal. Still, Varney withdrew money from his account in front of a crowd of eager spectators.

Image Source: Barclays

ATMs marked the beginning of self-service banking and paved the way for future digital innovations. The first ATM transaction signified something enormous for the industry: Customers could withdraw cash, check balances, and perform basic transactions outside of banking hours. According to the Financial Times, “the ATM blazed a trail towards today’s 24/7 ‘always-on’ culture.”

Now more than 50 years old, the ATM still has its fair share of fans, including Paul Volcker of the Federal Reserve, who famously called the ATM the “only useful invention in banking.”

Source: Cash and Dash by Bernardo Bátiz-Lazo

Today, ATM access still serves as a powerful differentiator for banking customers, especially those prioritizing efficient access to cash and low fees. Banks, credit unions, and fintechs are vested in securing the best ATM network deals and partnerships.

1970s — Credit becomes more accessible

Before the 1970s, American banks and credit card issuers could reject an applicant for being a woman, a person of color, or a religious minority. In 1970, the Fair Credit Reporting Act played a critical role in developing inclusive credit decisioning and a more transparent financial system.

In 1974, Congress passed the Equal Credit Opportunity Act, prohibiting credit discrimination based on a person’s sex, marital status, race, color, religion, country of origin, age, or government aid status. This legislation marked a significant step towards financial inclusion and equal access to credit in the US.

The same year, Roland Moreno patented the first smart card, a plastic card with a microchip that could securely store and process data. This innovation laid the groundwork for modern chip-based credit and debit cards, enhancing security and enabling more advanced transaction processing.

1990s — Online banking takes off

Online banking began in the 1980s but didn't take off until the internet became more accessible in the 1990s. As more and more customers learned they could access their bank accounts, transfer funds, and pay bills from home, digital banking experiences started to gain their foothold.

In the 1990s, fraud detection technology relied on traditional credit scoring and matching individuals' personally identifiable information (PII) to records in their databases. While these methods provided some level of protection, they were not always sufficient to keep up with fraudsters' evolving tactics. Consortium tools left gaps in fraud prevention coverage and were not well-suited to serve all markets effectively. Banks and credit unions recognized the need for more sophisticated and adaptable fraud detection solutions to safeguard their customers' assets and maintain trust in the digital banking environment.

How well do you know your fraud tech? Read about the evolution of fraud technology to find out.

2008 — The financial crisis accelerates fintech

The 2008 financial crisis exposed financial shortcomings that accelerated the rise of fintechs: technology providers offering digital-forward, customer-centric solutions to real-world banking problems.

Fintech startups introduced innovative financial services such as digital wallets, peer-to-peer lending, and budgeting apps, which traditional banks were slow to adopt. They disrupted the history of banking by leveraging technology to provide faster, more efficient, and user-friendly ways of handling finances.

2009 — Bitcoin is invented, catalyzing cryptocurrency

Bitcoin was invented in 2009, in what is widely considered a response to the lack of trust in traditional financial institutions and the perceived need for a more transparent and decentralized financial system. An anonymous person — or group — named Satoshi Nakamoto laid the foundation for cryptocurrency in a whitepaper titled "Bitcoin: A Peer-to-Peer Electronic Cash System." The whitepaper described secure, peer-to-peer transactions that forewent intermediaries like banks and governments by using a distributed ledger technology called blockchain that verified transactions across a network of computers.

For crypto fans, cryptocurrency offers a secure, efficient, and censorship-resistant alternative to traditional currencies. However, a lack of trust and information in crypto has slowed its adoption. Fraud has also been a deterrent, with fraud rings targeting cryptocurrency users in password hacking attacks, pig butchering scams, and account takeover attacks. Because cryptocurrency is unregulated, it has historically been difficult for victims to recover funds lost to fraud.

Despite these challenges, central banks are considering digital currencies to bolster financial inclusion and help citizens make more efficient payments. In 2016, Sweden became the first country to actively explore issuing a central-bank-backed digital currency, the e-krona, in preparation for a future without physical cash. Following this trend, El Salvador made history when it became the first country to adopt Bitcoin as a legal currency. To facilitate adoption, El Salvador created the Chivo Wallet app, where users can make deposits, withdrawals, and payments to peer and business bank accounts — in US dollars (El Salvador's official currency) and Bitcoin. These initiatives aimed to promote financial inclusion, bolster job creation, and facilitate remittances.

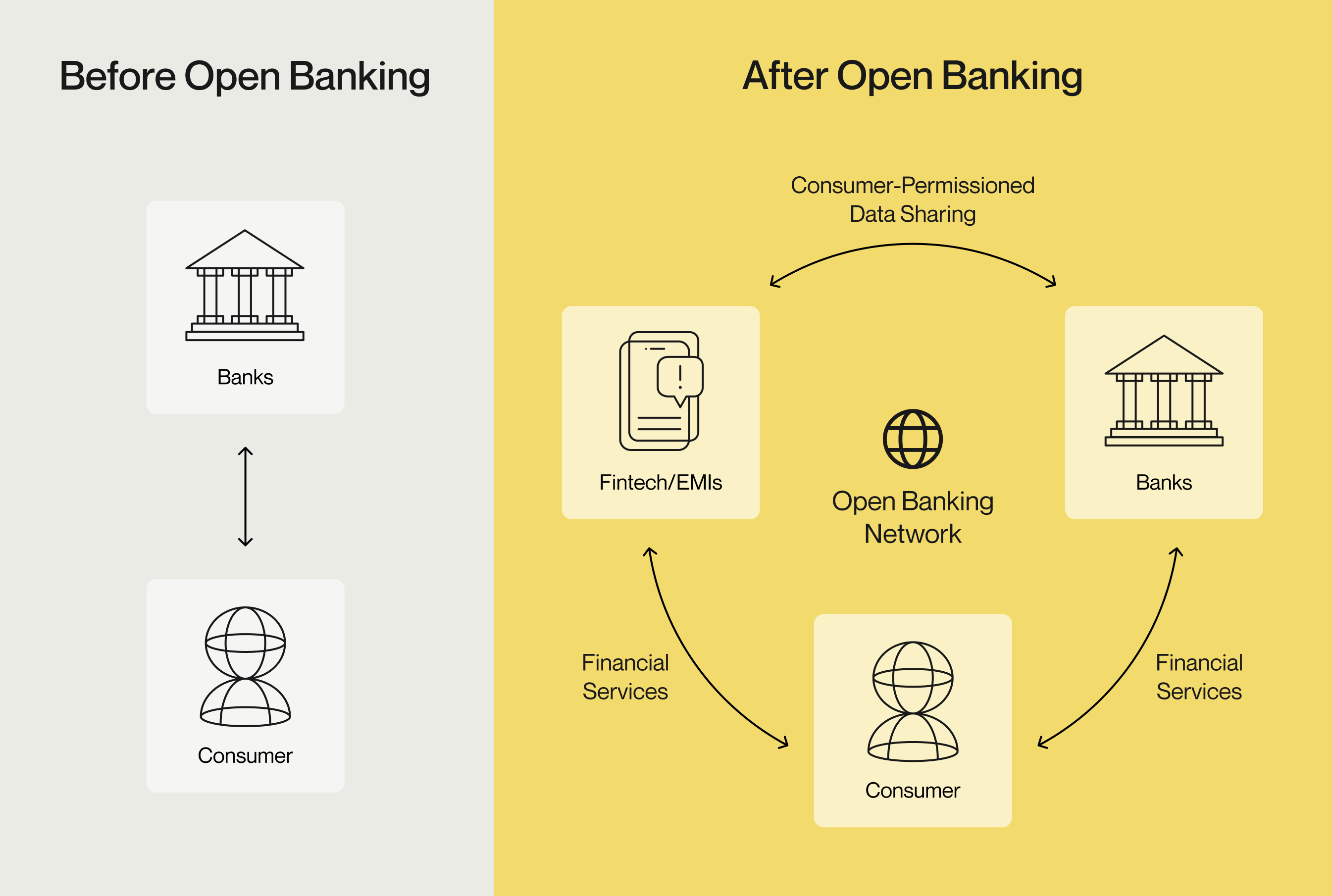

2018 — Open banking takes off as smartphone use grows

In 2018, the European Union mandated that banks are required to give authorized third-party providers access to their customers’ financial data at their customers’ request and with proper consent. This legislation, called the Revised Payment Service Directive (PSD2), ushered in open banking.

The PSD2 set a precedent for similar regulations globally, bolstering the growth of not just open banking, but embedded finance and banking as a service (BaaS) as well.

Open banking allows consumers to share financial data across apps and services. But like online banking before it, open banking also brought new opportunities for fraudsters to steal PII from consumers and businesses. To mitigate these risks, FIs enhanced their onboarding controls and increased monitoring throughout the customer lifecycle. Additionally, FIs adopted solutions to verify the legitimacy of third-party apps and services connecting to their systems.

Today, three-in-four consumers (76%) say that being able to connect apps and services is a top priority when choosing a bank. In the long run, open banking will create a more competitive, financially inclusive marketplace — as long as fraud remains a priority.

2020 — COVID-19 upsets in-person banking

The COVID-19 pandemic dramatically accelerated the adoption of digital payments as customers prioritized contactless and remote services for safety and convenience. Lockdowns, social distancing measures, and health concerns caused customers and businesses to avoid in-person financial transactions — with some avoiding cash altogether. With branches closing or operating at limited capacity, access to digital banking services became crucial for people awaiting government aid, unemployment benefits, and stimulus payments.

In 2020, banks and credit unions had to swiftly enhance their online and mobile offerings to meet the sharp surge in demand. Organizations already invested in extending their digital capabilities were better positioned to adapt, while others had to play catch-up.

Beyond payments, COVID’s tumultuous aftermath also highlighted the importance of inclusive financial services like credit underwriting for unbanked populations. An uptick in fraud demonstrated the growing need for more robust identity decisioning using both traditional and alternative data sources.

2024 — In-branch banking resurges as omnichannel popularizes

Banks and credit unions are reinventing the in-branch experience, combining technology with human expertise to provide a seamless omnichannel banking experience. To do this, they must strike the right balance of creating just enough friction to deter fraudsters but not enough to damage the onboarding experience or the quality of banking services.

Even as the world recovers from the crisis, customers who are used to the convenience and efficiency of digital banks are likely to continue expecting these services. Financial organizations must, therefore, continue to invest in their digital capabilities while also finding ways to provide the human touch and personalized support that customers value.

Today, customers expect a consistent experience across all banking channels. To do this, financial organizations need to address omnichannel’s unique challenges, including achieving smooth transitions between online and offline interactions, integrating data from various sources, and deploying responsive customer support across touchpoints. By delivering an exceptional omnichannel customer experience, financial organizations can differentiate themselves, build customer loyalty, and drive long-term success.

As banking evolves, so does fraud

Banks, fintechs, and credit unions count on Alloy to keep up

Fraud has been a persistent challenge throughout the evolution of banking. From temple looting to early paper forgeries to credit card fraud and mass-orchestrated AI fraud attacks, financial organizations have had to adapt their fraud prevention strategies to keep pace with a changing landscape.

To keep up, financial organizations must implement robust omnichannel security measures like advanced authentication, real-time fraud detection and monitoring systems, secure data encryption practices, regular audits, and both digital and in-branch vulnerability assessments. For banks, credit unions, and fintechs of the present, partnering with a specialized omnichannel provider like Alloy can help.

Alloy is an Identity Risk Solution that offers fraud risk management at onboarding and throughout the customer lifecycle. Our platform leverages data from 200+ trusted vendors and advanced machine learning to enable real-time identity verification, fraud detection, and risk assessment. We’re constantly improving our solution to grow with you — even as the industry evolves.

Alloy helps your financial organization make informed identity decisions quickly and accurately.

KJ McAlpin is a Senior Content Marketing Manager, Fraud Strategy at Alloy, where they specialize in writing about fraud prevention, regulatory compliance, and innovation in financial services. With a focus on helping financial institutions and fintechs navigate an evolving risk landscape, KJ highlights trends shaping the future of identity, fraud, and regulation. Outside of work, they enjoy traveling, journaling, and spending time with their two black cats.

{kind=link}