When and how to file a Suspicious Activity Report (SAR)

Mar 27, 2023

Alloy’s SAR filing feature makes it easy to report suspicious activity

Banks must monitor their customers to ensure that they aren't depositing "dirty money" (proceeds from illegal activity) into the bank or using the American banking system to commit crimes like terrorist financing. Once a bank determines that a transaction or series of transactions meets federal reporting requirements, the bank files a Suspicious Activity Report (SAR).

Federal law requires certain financial institutions (FI) operating in the United States to file a SAR no later than 30 calendar days after the date the FI initially detected suspicious or unusual activity. If you are a fintech working with a partner bank subject to SAR requirements, then you will likely be on the clock as well.

What is a Suspicious Activity Report (SAR)?

A SAR is a tool provided under the Bank Secrecy Act (BSA) for monitoring activities that give rise to a suspicion that an account holder is using the account to commit a crime — such as money laundering, terrorist financing, and human trafficking — or hold the proceeds from criminal activity.

The Financial Crimes Enforcement Network (FinCEN) regulates who must file a SAR, when SARs must be filed, what information must be included on the SAR, the form the SAR must take, the procedures regulators follow when examining whether an FI is appropriately doing all of the above, and the consequences for failing to follow federal law in this area.

Who must file a SAR?

Generally speaking, banks, casinos, money services businesses (MSBs), brokers/dealers, and other licensed financial institutions listed in this FinCEN guidance document are obligated to file a SAR within 30 calendar days of detecting the suspicious activity (this can be extended to 60 days if the subject of the SAR is unknown).

If you are a fintech without a banking license, you likely will have contractual obligations with your partner bank (i.e. the filing institution) to provide them details of suspicious activity that takes place at your organization.

What constitutes “suspicious activity”?

In some ways, the sky's the limit. It varies widely based on a bank's process for detecting suspicious activity.

For example, suppose an 80-year-old grandma on Social Security suddenly starts having all her deposits made by her grandson, who is now depositing $9,000 in cash weekly. In that case, the bank should investigate the account and possibly file a SAR, close down the account, or both. (Spoiler: He may be a drug dealer).

On the other hand, a legitimate business person making $9,000 deposits may not be a problem. Context is crucial.

What is at stake?

With heightened regulatory scrutiny, financial institutions can face significant fines and penalties for failing to file suspicious activity reports on time. Organizations can also face reputational damage and loss of clients due to non-compliance.

It's also worth noting that once filed, SARs are confidential, and it is illegal to reveal the existence of a SAR to the subject or any third parties. The penalties for disclosing information around filed SARs can include hefty penalties and even jail time.

How does SAR filing work?

Completing a SAR can often be complex, with a multitude of fields to input and case details to reconcile. The process can also be tedious and prone to error due to the manual nature of the data collection, especially when there are multiple systems to be checked. This is why it's important to have a robust compliance monitoring system in place to flag and act upon risky activity in a single platform.

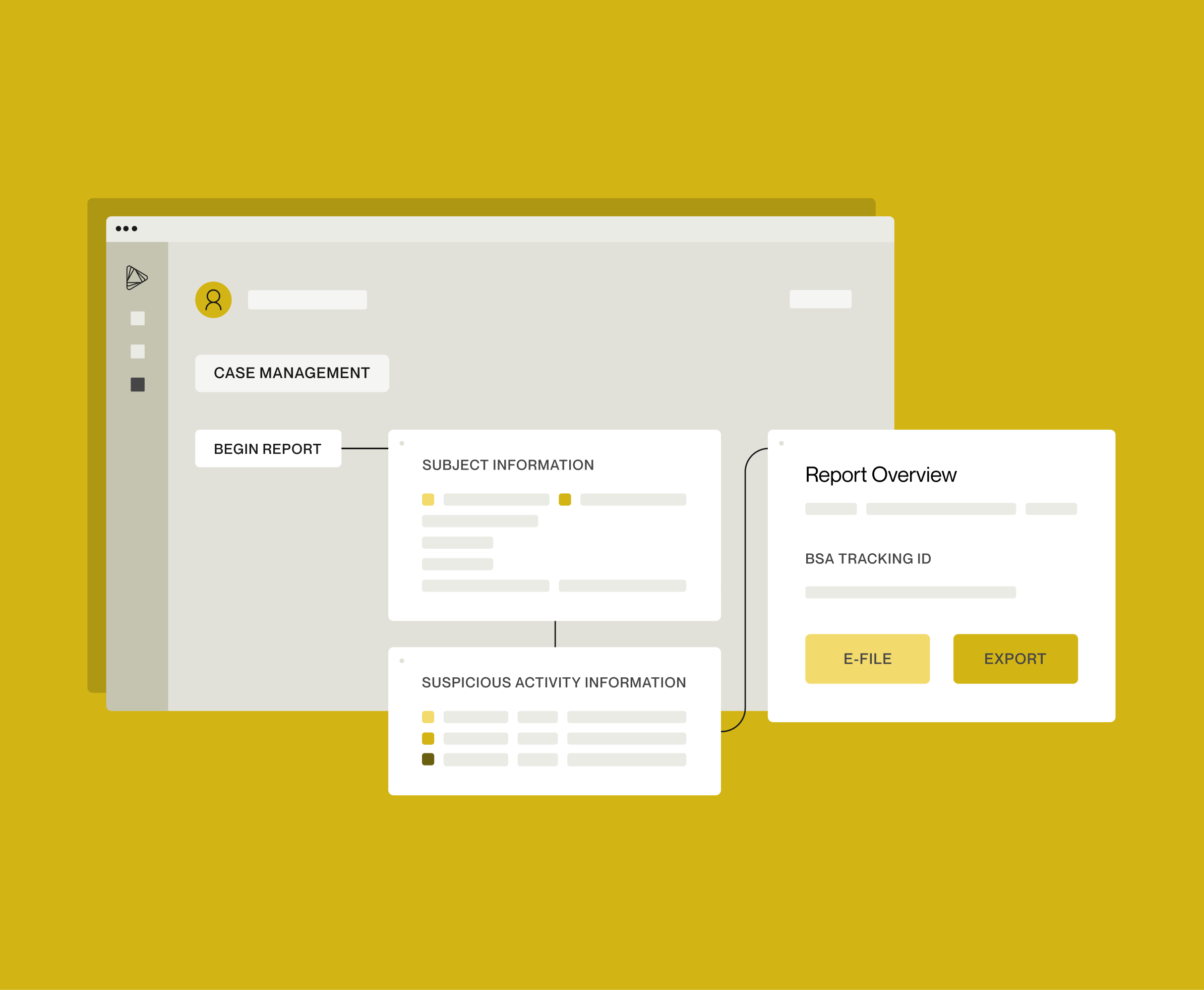

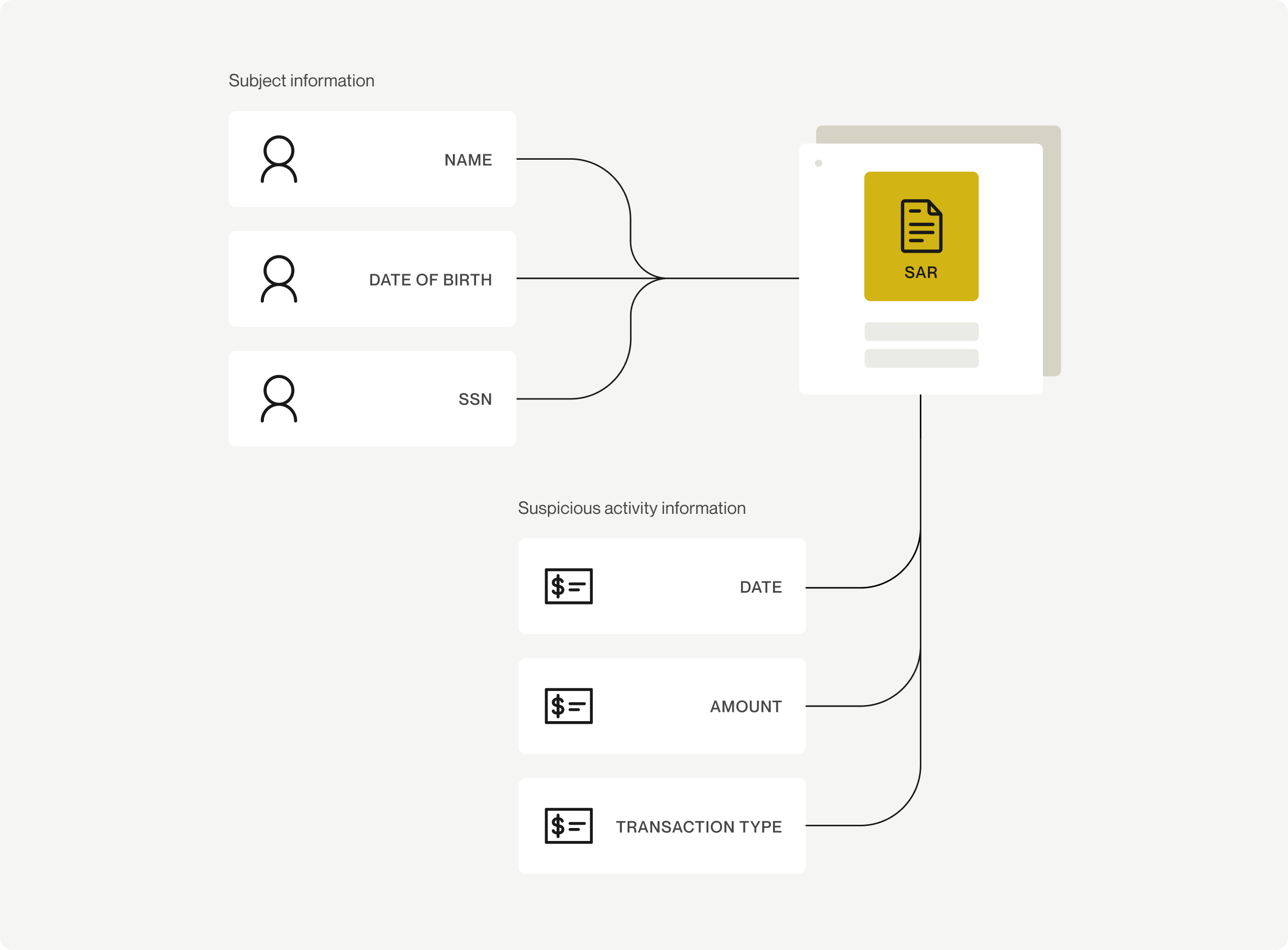

How can Alloy help with your SAR needs?

Alloy's SAR filing tool can help you satisfy your regulatory obligations more efficiently by enabling clients to file a report right within our case management system.

Alloy prepopulates transaction and subject details, simplifying data entry for your compliance officers. Because the SAR filing tool is built into Alloy's case management system, your teams have direct insight into the entity's complete historical activity and any other contextual evidence that may be required for SAR due diligence.

Prior to submission, Alloy will validate the fields to catch any errors which may result in the report being rejected by FinCEN. The end result is an aggregated report which can be e-filed directly with FinCEN. Alloy's system also captures FinCEN's confirmation of receipt, so you track the progress of your filings directly from the dashboard.

Alloy can help you with your compliance needs

Clint Heyworth is the Director of Compliance at Alloy and brings almost 20 years of experience in the field to the company. After leaving private practice, he was Senior Director of Compliance at PLS Financial Services, CCO, ISO, and in-house counsel at Sutton Bank, and CCO at Greenlight.