Is fraud just another cost of doing business?

Jul 17, 2025

The cost of fraud is growing, but so are fraud prevention abilities

Many executives write off fraud as just another cost of operating their financial institution or fintech. But at 87%, an overwhelming majority of fraud decision-makers agree that the amount of money their organization saves by mitigating potential fraud losses outweighs the cost of fraud prevention. In fact, some organizations, such as Consumers Credit Union, have found that every dollar invested in fraud prevention yields a $5 return on investment.

While fraud is, beyond a doubt, something all financial institutions and fintechs must factor into revenue projections, we wanted to ask: Is fraud actually a cost center that financial service providers must accept? Or is fraud an expense that organizations can actually strive to minimize, or even eliminate, with the right strategy?

The direct and indirect costs of fraud

Fraud expenses fall into two categories — direct and indirect costs.

Direct costs: actual money lost to fraud

Direct fraud costs refer to the amount of money lost when someone successfully defrauds a financial institution. Financial organizations say that direct losses are growing despite increased investment in prevention measures.

Indirect costs: nonmonetary impacts with financial consequences

Indirect fraud costs refer to any losses related to a fraud attack, but not the direct result of financial theft. They can be anything from fraud investigation and recovery expenses to prevention costs, interest, and regulatory penalties. Other examples of indirect costs include a reduction in customer growth brought on by tightened security measures and loss of clients brought on by a poor user experience.

According to LexisNexis Risk Solutions' True Cost of Fraud Study, every dollar lost to fraudsters in 2024 cost financial organizations an average of $4.76. To put this into perspective, this multiplier effect means that a $100 fraud loss actually costs organizations $476 when considering interest, fees, and recovery expenses.

For lending institutions, this impact is even more pronounced: Each dollar lost to fraud represents $5.16 in total costs. These numbers underscore the fact that what appears as a simple dollar-for-dollar loss on paper quickly balloons into a much larger financial burden that affects multiple aspects of the business.

To understand how indirect fraud costs can manifest as actual dollars, we can begin by examining one of the most clearly documented types of fraud expenses: regulatory fines and penalties.

According to Finbold, financial institutions were forced to pay over $4.5 billion in regulatory fines globally in 2024. The steepest penalties were imposed by US regulators, who assigned $4.08 billion in fines between 19 cases. Although they represented only a third of the cases, penalties paid to US regulators accounted for 90% of total fines.

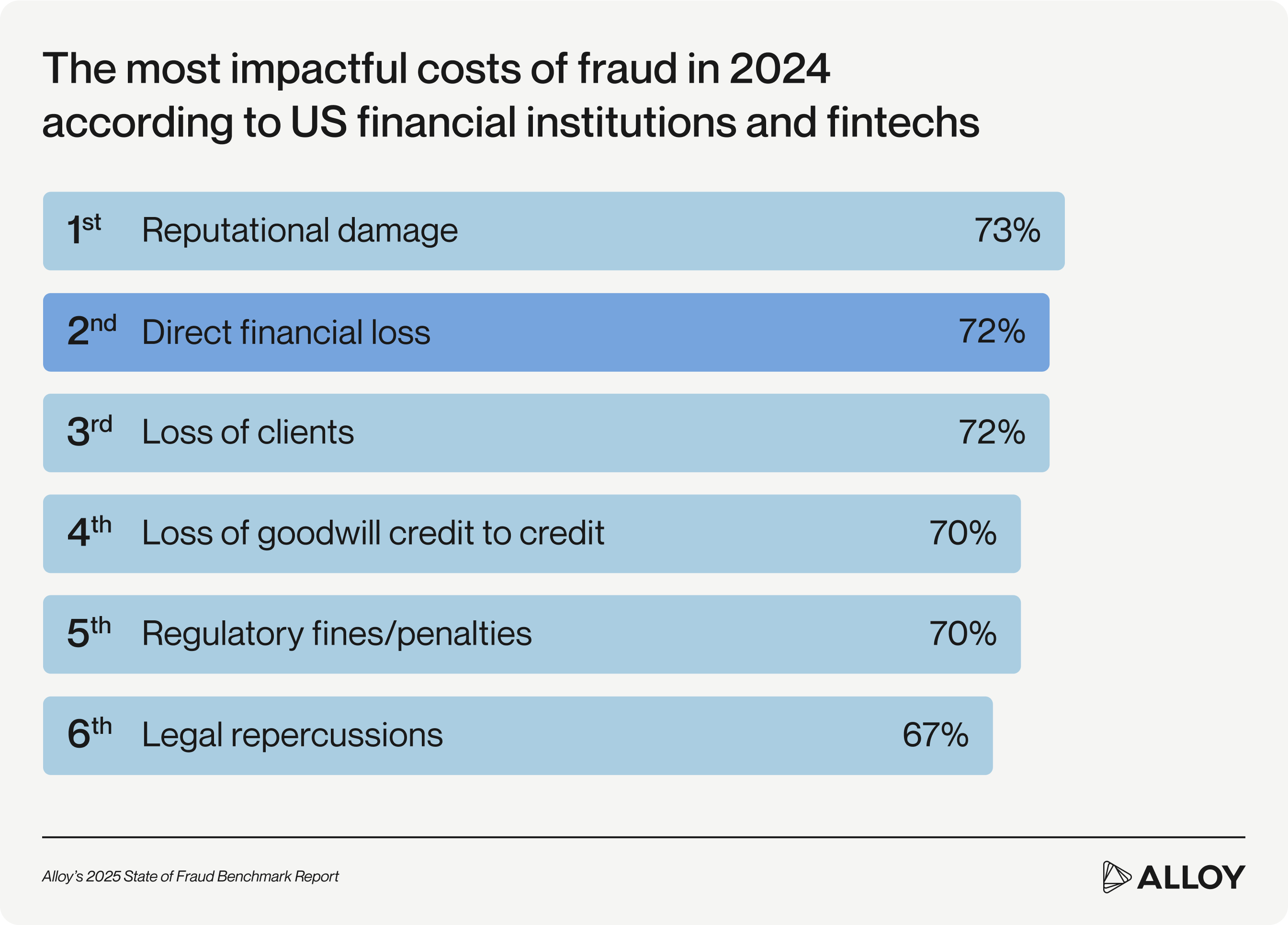

Despite the cost of direct fraud losses and regulatory penalties, a majority of fraud decision-makers at financial organizations agreed that reputational damage was their top concern following a fraud incident (73%).

Reputational damage can be hard to quantify. However, in today's social media-informed world, where customer complaints can quickly go viral, a single successful fraud attack can erode customer trust on a broad scale. The consequences of reputational damage may affect not just customer retention and acquisition, but also partnerships, making it an even more significant blow than the loss itself.

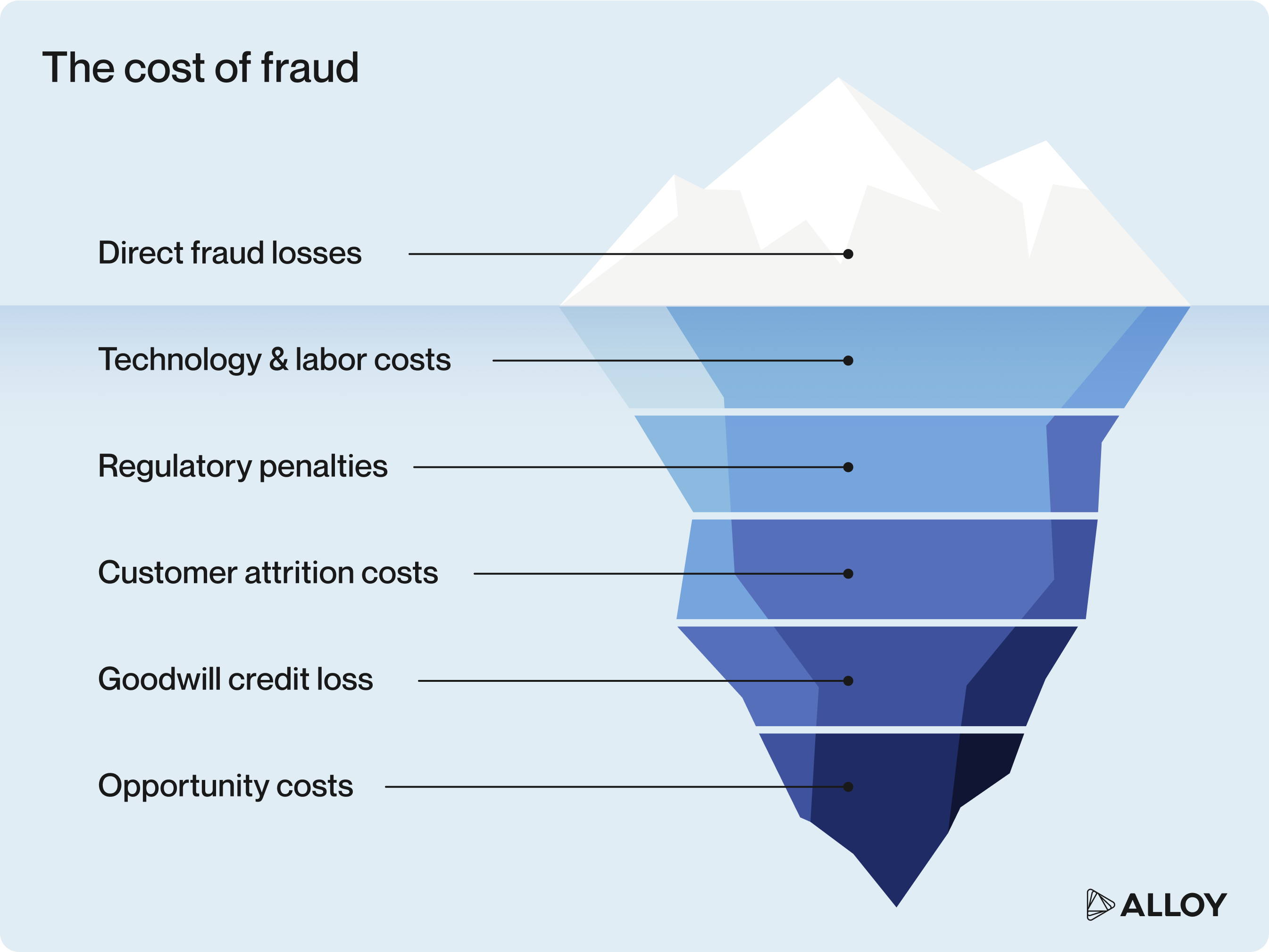

What are the drivers of fraud costs?

Calculating the total cost of fraud involves adding direct fraud costs to any regulatory penalties, as well as technology and labor costs. It also involves factoring in harder-to-track elements, such as customer attrition, loss of goodwill credit, and opportunity costs (such as when marketing spend has to be diverted and new channels shut down as a result of a fraud attack).

To consider the full scope of fraud costs outside of direct losses also requires us to look at fraud cost drivers. Here are some of the key factors driving fraud costs, and how financial institutions and fintechs are experiencing them firsthand.

The size factor

When it comes to fraud losses, the size of a financial organization makes a difference. According to fraud report data, enterprise banks experienced the most significant growth in fraud in 2024, with nearly 70% reporting an increase in fraud over the past year. But credit unions and other mid-sized financial institutions face their own unique challenges, often experiencing lower absolute fraud losses but higher relative impact on their bottom line.

Having more assets under management (AUM) also means anticipating greater fraud costs. In our recent benchmark report, enterprise banks reported the highest volume of direct fraud losses.

A financial organization’s size may also affect which type of fraud costs it finds the most consequential. For example, our data shows 80% of enterprise banks cited reputational damage as their top concern following fraud incidents, while mid-market banks reported goodwill credit losses as their largest consequence (69%). These differences underscore the importance of tailoring fraud prevention strategies to an organization's specific scale, customer base, and operational model.

In 2024, nearly 2 in 5 UK fintechs reported experiencing fraud losses ranging from £1 million to £5 million. Despite significant direct fraud costs, regulatory fines and penalties are the primary concern for this sector.

Time is money, especially in fraud detection

The speed at which fraud is detected also matters when calculating the total cost impact on financial organizations.

Decision-makers at financial institutions and fintechs most commonly detect fraud in real-time during transactions. Catching fraud in real-time during transactions often means that fraudsters have already gained some form of account access, but the funds may not have left the institution yet.

The cost implications of detection at different stages vary dramatically:

- During onboarding — Onboarding is the earliest point at which financial institutions and fintechs can detect fraud. This also makes it the best time for stopping new account fraud and synthetic identity fraud: Before bad actors pass their initial identity check and get assigned a risk level. This proactive strategy often requires upfront investment in identity verification technology, but yields significant savings by preventing fraud risk in the first place. Enterprise banks lead this approach, with 38% detecting most fraud during new account onboarding.

- At the time of transaction — Most financial organizations (56%) identify fraud after account creation, when a suspicious transaction triggers alerts. While this approach can prevent fraudulent digital payments, it often comes after access to the account has been granted. Recovery costs and potential reputational damage are higher than with onboarding detection, but fraud mitigation is still possible.

- After the fact (recovery) — When fraud is discovered after transactions have completed, financial institutions face the highest costs. Beyond direct monetary losses, organizations must allocate significant resources to investigating fraud schemes, pursuing legal action, reimbursing customers, and managing reputational fallout. Recovery rates at this stage of fraud management are typically low.

Most financial institutions and fintechs monitor for fraud either at onboarding or at transaction time, but not both. With less than half (47%) of financial institutions and fintechs monitoring applications and transactions in real-time, blind spots like these can result in greater vulnerabilities. Organizations implementing monitoring across the entire customer lifecycle are more likely to prevent these types of losses from occurring.

Regulatory trends affect fraud-related penalties

As policymakers call for greater accountability from financial institutions and fintechs, global regulators are increasingly focused on anti-money laundering (AML) compliance and transaction fraud. The high-profile examination of Zelle's fraud reimbursement policies has highlighted a growing expectation for transparency and consistency in how financial organizations address fraud losses.

Regulatory response to cybercrime and emerging fraud trends can substantially impact fraud costs, with penalties targeting banks surging 522% to $3.65 billion in 2024. Transaction monitoring violations — which span both fraud and money laundering detection — saw penalties exceeding $3.3 billion, representing a 100% year-over-year increase between 2023 and 2024.

Today’s regulators are cracking down on money laundering at a significant cost to financial organizations. Last year, TD Bank was ordered to pay $3.09 billion in penalties for charges related to money laundering. This single fine accounted for nearly 69% of the total cost of global regulatory penalties. Meanwhile, in Europe, Sweden’s Klarna Bank was hit with a $46 million penalty for AML violations. This discrepancy in fines shows how the cost of fraud varies not only by financial organization, but also by jurisdiction.

Recommended reading: How to tackle the challenges of AML monitoring

Automation can curb losses

Artificial intelligence (AI)-powered fraud automations can help stop fraud losses from happening. Rather than relying on manual reviews that can take hours or days, actionable AI tools can identify suspicious patterns and block potentially fraudulent transactions in milliseconds.

Nearly all (99%) of financial institutions and fintechs now use machine learning, a form of AI, as part of their fraud prevention strategy. The most common applications include:

- Providing explainability for large data sets (67%)

- Supplementing rule-based decisioning with supervised machine learning models (59%)

- Automating operations and investigations (59%).

This near-universal adoption reflects a fundamental shift in how the industry approaches fraud detection.

AI-based systems can quickly run data analytics, analyzing thousands of data points simultaneously to identify subtle patterns that would be impossible for human analysts to detect. The specific ways automation reduces fraud costs include:

- Reduced false positives — Machine learning models become increasingly accurate over time, meaning fewer legitimate transactions are flagged as suspicious. This decreases operational costs and improves customer satisfaction.

- Faster detection — AI systems can identify and respond to potential fraud in real-time, often before transactions are completed. This real-time capability is particularly valuable when combating fraud attempts that come from financial crime rings.

- Operational efficiency — Automation reduces the need for manual review of suspicious activities, allowing staff to focus on more complex cases and strategic initiatives.

- Pattern recognition across accounts — AI can detect coordinated fraud attacks by recognizing patterns across seemingly unrelated accounts, something that's extremely difficult with manual review processes.

This widespread adoption addresses the automation gaps that stand in the way between fraud detection and fraud prevention.

Balancing customer experience with risk

The number one thing holding financial institutions and fintechs back from offering seamless customer experiences, such as instant payments isn't the technology itself. It's the fear of fraud.

Overly restrictive security measures drive up operational expenses through increased manual reviews and customer support calls. These same measures can significantly impact the customer journey, resulting in reduced revenue through abandoned applications and decreased product usage. At the same time, not having enough customer friction means there’s nothing to keep fraudsters from riding out a scam till the very end.

Enabling digital banking features (such as Zelle and wires) is difficult only because it's risky. But risk management doesn't have to be the department of "no." The most forward-thinking financial organizations are flipping the script by treating fraud prevention not as a cost center but as a business enabler.

To pull this off, financial institutions and fintechs need the flexibility to implement contextual, risk-based approaches that apply friction only when something looks genuinely suspicious.

Is fraud really just another cost of doing business?

The answer is, yes and no.

The primary purpose of financial institutions and fintechs is to store and transmit money safely and securely, so preventing fraud is an integral part of their mandate.

However, it's important to recognize that not all money spent is money lost. Investing in fraud prevention upfront will save you from considerable direct fraud costs. Plus, it can help prevent some of the more expensive, yet indirect, costs of fraud that may occur in the future.

Some indirect costs — such as those necessary to prevent, detect, and mitigate fraud — should always be included in your budget. Then again, so should buying locks for your doors. Perhaps this is why 64% of financial institutions and fintechs plan to invest in an identity and fraud prevention platform within the next year.

Reducing fraud costs starts with robust prevention

Nearly all financial organizations (93%) report ongoing investment in fraud prevention in 2025. The most effective fraud prevention investments are identity and fraud prevention platforms that leverage multiple detection and prevention tools — like automated step-up verifications, alternative datasets, and machine learning. These are available from one central console, which fraud teams can use to monitor fraudulent behaviors and identities at onboarding and throughout the customer lifecycle.

Identity and fraud prevention platforms like Alloy combine:

- Real-time transaction monitoring that evaluates each transaction against evolving risk models

- Adaptive authentication systems that apply appropriate friction only when needed

- Behavioral data analytics that detect subtle changes in customer patterns, indicating account takeover

- Network analysis tools that identify connections between seemingly unrelated suspicious activities

A robust fraud prevention and management system can directly reduce the number of bad actors that slip through your fraud controls, thereby increasing your chances of stopping them. It will also drive down direct and indirect fraud costs, like legal repercussions, regulatory fines, and reputational damage.

When you have the right tools and people behind your fraud controls and processes, fraud is no longer a “lost cost” — it’s a strategic differentiator between you and your competitors.

Learn how Consumers Credit Union saves $5 for every $1 spent on fraud prevention

Stay ahead of fraudsters and competitors

Explore data-backed strategies from financial institutions that are winning the fraud prevention game in our 2025 benchmark report.

KJ McAlpin is a Senior Content Marketing Manager, Fraud Strategy at Alloy, where they specialize in writing about fraud prevention, regulatory compliance, and innovation in financial services. With a focus on helping financial institutions and fintechs navigate an evolving risk landscape, KJ highlights trends shaping the future of identity, fraud, and regulation. Outside of work, they enjoy traveling, journaling, and spending time with their two black cats.