How Alloy helps credit unions rival enterprise banks on security

Oct 1, 2025

Fraud rings move fast. Once they discover a vulnerability, the details can spread across networks of bad actors in hours — sometimes overnight — triggering coordinated attacks on multiple institutions.

Credit unions, with their community-driven focus and often smaller fraud teams, face the same sophisticated threats as enterprise banks but without the same level of in-house resources. And attackers know how to take advantage of the vulnerabilities common to many credit unions: siloed systems between digital and branch operations, slower detection of emerging patterns, and gaps in real-time intelligence sharing. When one credit union’s defenses are breached, others with similar setups become easy secondary targets.

To match the security posture of larger players, credit unions need access to the same caliber of fraud prevention technology — tools that detect patterns early, connect every member touchpoint, and scale without adding headcount. Delivering a combination of AI-powered fraud models, real-time data orchestration, and a networked approach to threat intelligence, Alloy gives credit unions the protection and agility they need to rival enterprise financial organizations.

How do fraud rings target credit unions?

Today’s fraud attempts aren’t typically driven by isolated bad actors. More often, they’re executed by highly organized rings running coordinated campaigns. Seven in 10 financial organizations now attribute most fraud attempts to sophisticated criminal groups.

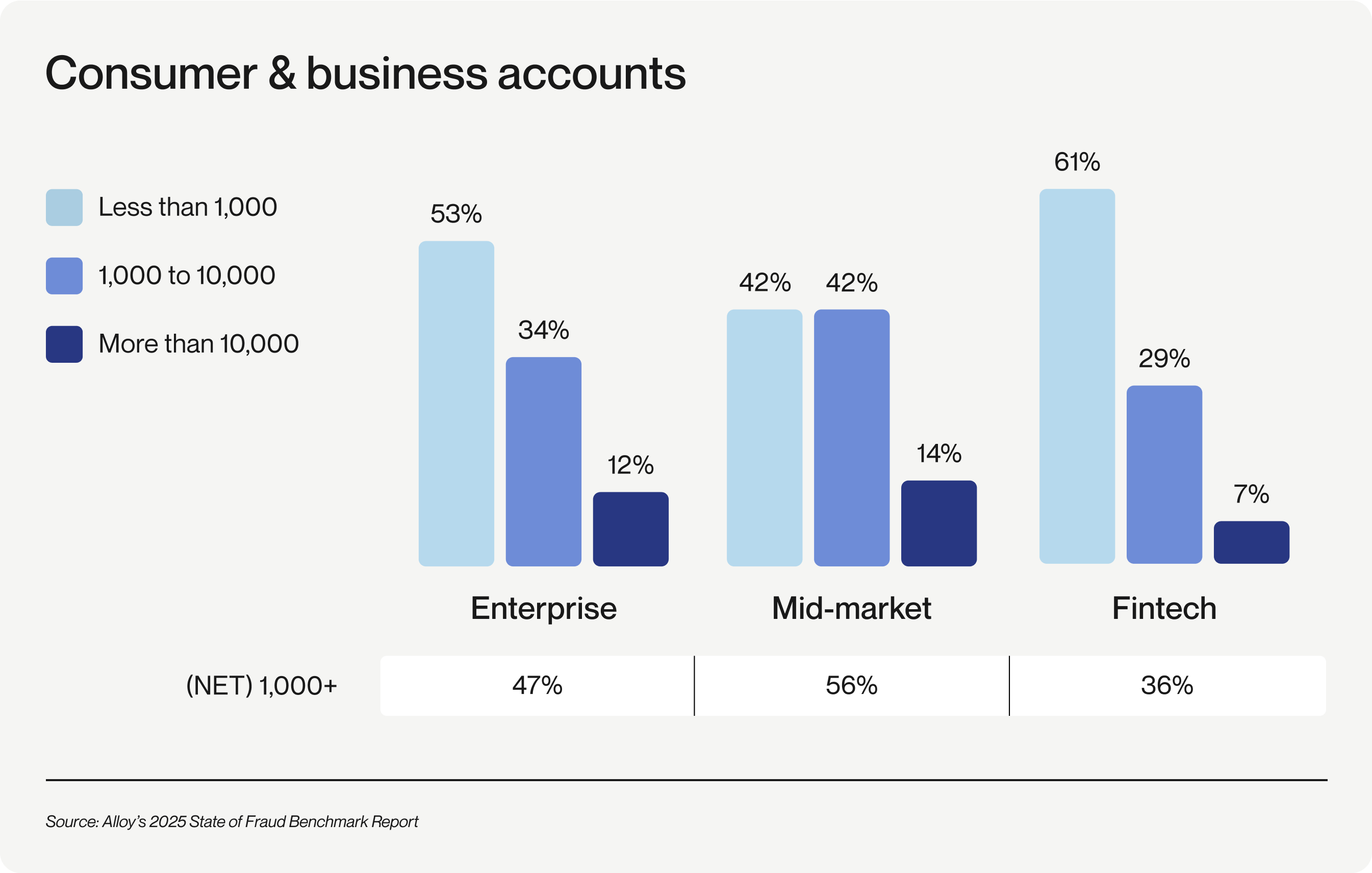

In Alloy’s 2025 State of Fraud Benchmark Report, credit unions — grouped with other mid-market banks in the data — reported the highest levels of fraud on average. More than half (56%) experienced over 1,000 fraud cases in 2024 — higher than any other segment.

Source: Alloy’s 2025 State of Fraud Benchmark Report

One reason credit unions are targeted by fraudsters may be a matter of perception. Enterprise banks are seen to have stronger fraud defenses, making fraudsters more likely to test smaller institutions they view as easier marks.

For credit unions, these aren’t small-dollar incidents. Credit unions were the only institutions to report fraud losses above $5M, with some exceeding $10M.

The financial impact matters, but the bigger risk is reputational. Account takeover and identity theft together made up nearly half of all reported fraud cases. An account takeover can lock a member out of their account, trigger missed bill payments, and force hours of identity re‑verification. Identity theft can damage credit, jeopardize loan approvals, and create lasting anxiety. These are exactly the kinds of experiences that erode member trust — the foundation of what makes credit unions different.

Why traditional approaches aren’t enough

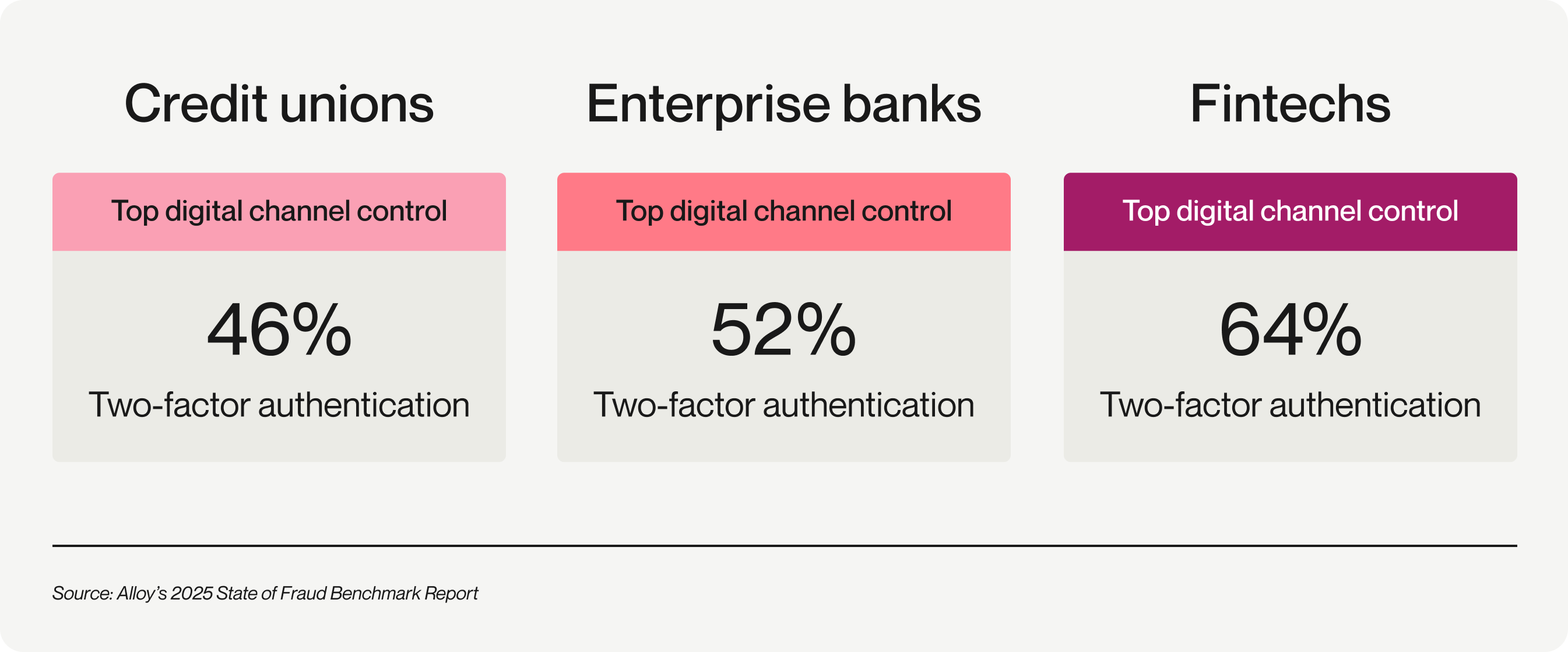

According to Alloy’s report, 80% of fraud now occurs in digital channels. However, credit unions lag behind other financial organizations in implementing automated step-up controls like 2FA, with only 46% of credit unions using these controls as a first line of defense.

Step-up authentication is a security measure that requires users to provide additional authentication when their behavior appears risky or unusual, such as logging in from a new device, making large transactions, or accessing sensitive information. These controls dynamically "step up" the level of verification required based on the risk level of the activity.

Source: Alloy’s 2025 State of Fraud Benchmark Report

Detection is also happening too late. Among credit unions and other mid-market institutions, only 33% most commonly detect fraud at onboarding, while more than half (56%) catch it only once a transaction is underway. That leaves fraudsters inside the system before defenses kick in — an expensive and avoidable gap.

These reactive processes slow down member onboarding, create friction for legitimate applicants, and still leave room for fraud to slip through.

How Alloy gives credit unions enterprise-grade protection

Alloy was built to close that gap. The platform brings together data, automation, and intelligence so credit unions can fight fraud with the same sophistication as the largest banks — without needing enterprise-sized budgets or teams.

Protection at onboarding and throughout the customer lifecycle

Despite credit unions’ focus on the onboarding process, only 33% of credit unions report catching fraud most commonly at onboarding, with a majority identifying it later on at the transaction stage.

Enterprise banks are further ahead, with 38% detecting fraud most often at onboarding — the highest of any sector. Institutions that stop bad actors early keep them out of the system entirely, while credit unions remain more likely to discover fraud only after it has already occurred.

Alloy helps close this gap by maintaining a dynamic risk profile for every member, continuously updated with signals from onboarding through every touchpoint in the relationship.

Shared intelligence

Fraudsters don’t stop at the walls of a single credit union. They move from one institution to another, probing for weaknesses until they find an entry point. That’s why going it alone leaves credit unions at a disadvantage.

Alloy changes that by creating a layer of shared intelligence across its network. By working with more than 700 financial institutions and fintechs worldwide, Alloy combines insights that credit unions can use to strengthen their defenses and define best practices for their own institutions.

Just as important, Alloy facilitates direct conversations between credit unions by hosting regular summits. These gatherings give fraud and risk leaders a forum to share experiences, compare strategies, and learn from one another in real time — extending the sense of community that credit unions are built on into their fraud prevention efforts.

New and emerging risk signals from across Alloy's industry-spanning platform can be used to strengthen defenses. For credit unions, this means access to enterprise-grade insight without enterprise budgets — collective intelligence that helps them recognize coordinated attacks faster and protect members more effectively.

Discover our upcoming summits and events

Automation that scales

Credit unions often face resource constraints: fraud teams are small, budgets are limited, and manual reviews eat up valuable staff time. That makes it hard to deliver the fast, seamless experience members expect while keeping fraud out.

Alloy levels the playing field with enterprise-grade automation, replacing manual checks with real-time decisions across applications and transactions. Instead of pulling staff into every flagged application or transaction, Alloy runs real-time decisions across both — applying the same rigor whether your credit union is processing dozens of applications a day or thousands.

The result is fraud controls that scale with your membership. Credit unions can expand services and grow their base without adding proportional headcount or sacrificing security — a true democratization of the tools only the largest institutions used to afford.

Making it work in practice

Eighty-seven percent of financial organizations say the savings from fraud prevention outweigh its cost. The ROI of fraud prevention is clear — but how do you actually get there?

For most credit unions, success with Alloy comes from starting small and building in phases.

Consumers Credit Union followed this path. It began by transforming digital onboarding, where fraud losses and manual reviews were creating the most pain. Once that process was automated and stable, it expanded Alloy into in-branch workflows to close gaps fraudsters were exploiting. Now, they’re extending Alloy into business onboarding and document verification — a steady expansion that keeps members protected across every channel.

This phased approach delivers early wins without overwhelming teams or budgets, and the results compound quickly. At Consumers, every dollar spent on Alloy has saved five times more in fraud losses.

Automation is the other critical piece. By letting Alloy handle routine reviews and policy enforcement in real time, credit unions free staff to focus on strategy and member service instead of chasing down alerts. That combination — phased rollout plus scaled automation — is how credit unions make fraud prevention work in practice.

From first touch to lifelong trust

Member protection goes beyond preventing financial losses or blocking fraud attempts. It's fundamentally about safeguarding the trust that credit unions have cultivated over generations. Success means striking the right balance — preventing fraud while maintaining the seamless experience members expect.

Alloy makes that possible. By combining shared intelligence, onboarding, lifecycle monitoring, and real-time interdiction, Alloy enables credit unions to deliver enterprise-grade security while keeping the member experience seamless.

Talk with us about building stronger fraud defenses for your members

Alloy connects credit unions to 250+ data solutions across 195 markets. That reach means your team can spot coordinated fraud faster, cut down on manual reviews, and give members the secure, seamless experience they expect.

KJ McAlpin is a Senior Content Marketing Manager, Fraud Strategy at Alloy, where they specialize in writing about fraud prevention, regulatory compliance, and innovation in financial services. With a focus on helping financial institutions and fintechs navigate an evolving risk landscape, KJ highlights trends shaping the future of identity, fraud, and regulation. Outside of work, they enjoy traveling, journaling, and spending time with their two black cats.