Delivering a friction-right banking experience

Aug 18, 2025

Learn how Alloy keeps accounts safe without sacrificing CX

Fraud risk strategies have been known to negatively impact the customer experience (CX). But for the financial institutions and fintechs using Alloy, it’s possible to prevent fraud while also delivering a seamless experience to end-users.

To illustrate how we make this possible, let’s dive into the perspective of a customer and a fraudster who are each trying to access the same bank account protected by Alloy.

Scenario 1: The legitimate customer

Emergencies can happen anywhere — on the go or close to home. And when they do, customers expect speedy, seamless, and secure experiences from their financial organization.

The Smith family’s dog gets sick while they are vacationing in Costa Rica. Mrs. Smith needs to send an emergency transfer to the pet sitter to cover the vet bills.

Here’s what this process looks like from the customer’s perspective as well as what’s happening behind the scenes at her bank.

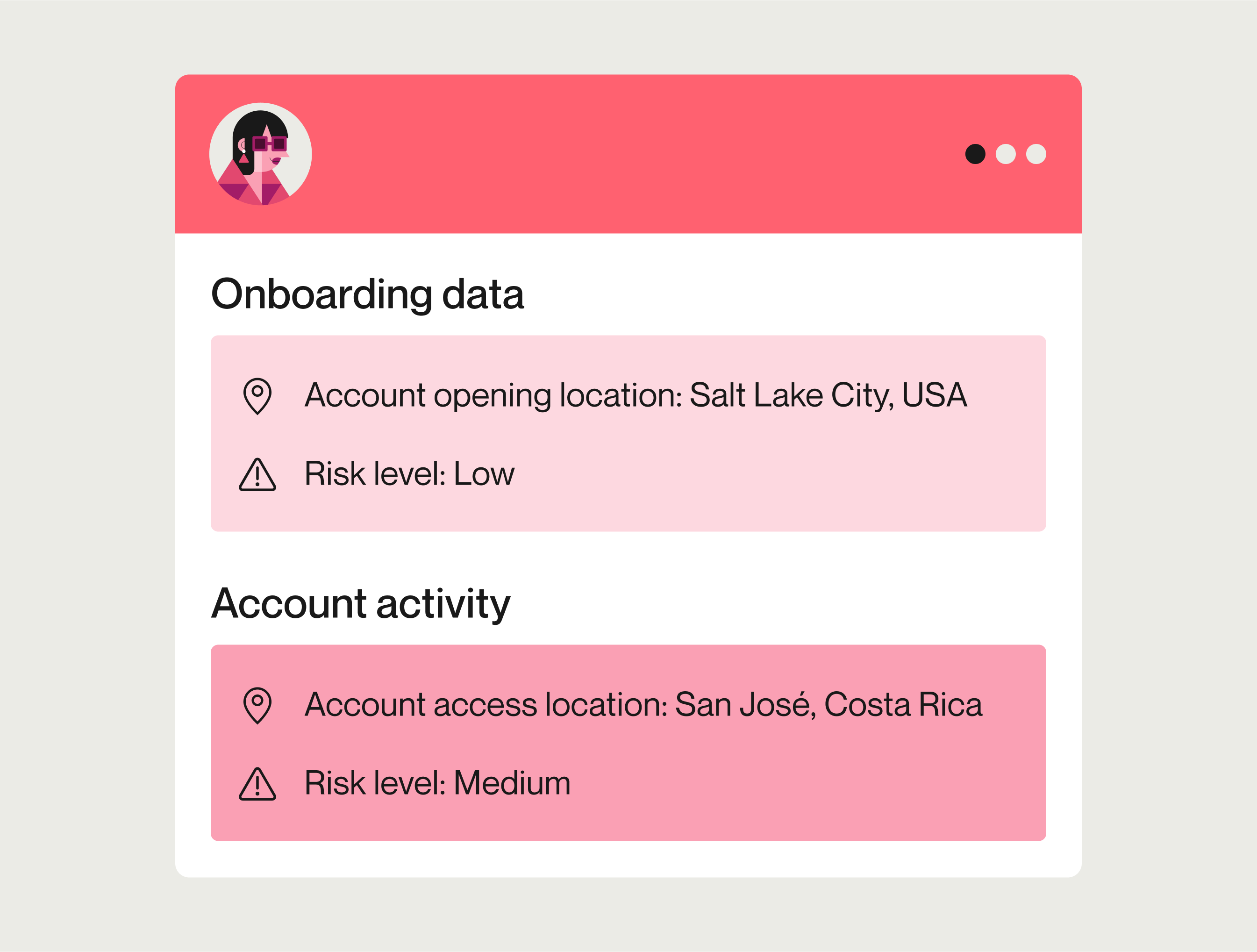

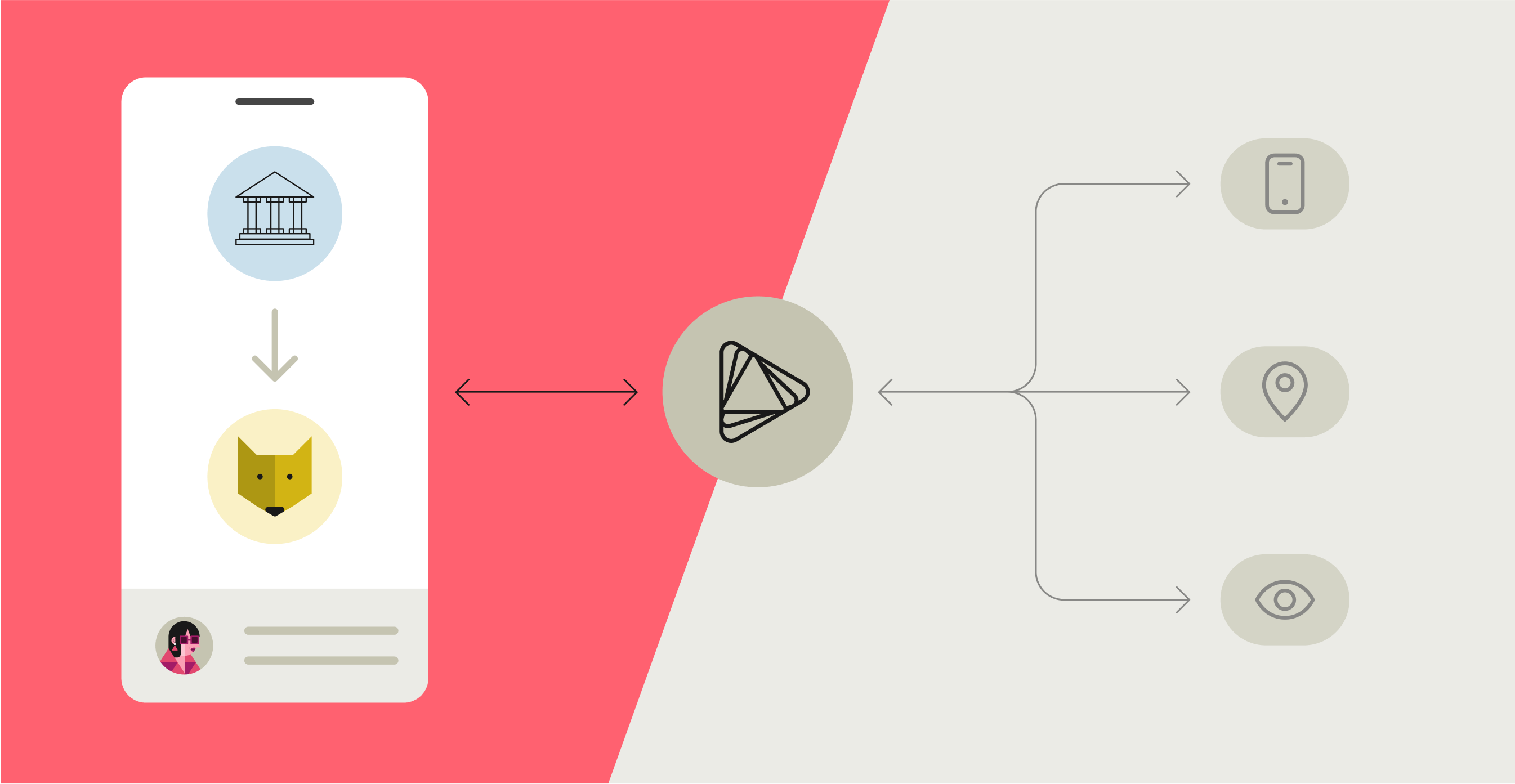

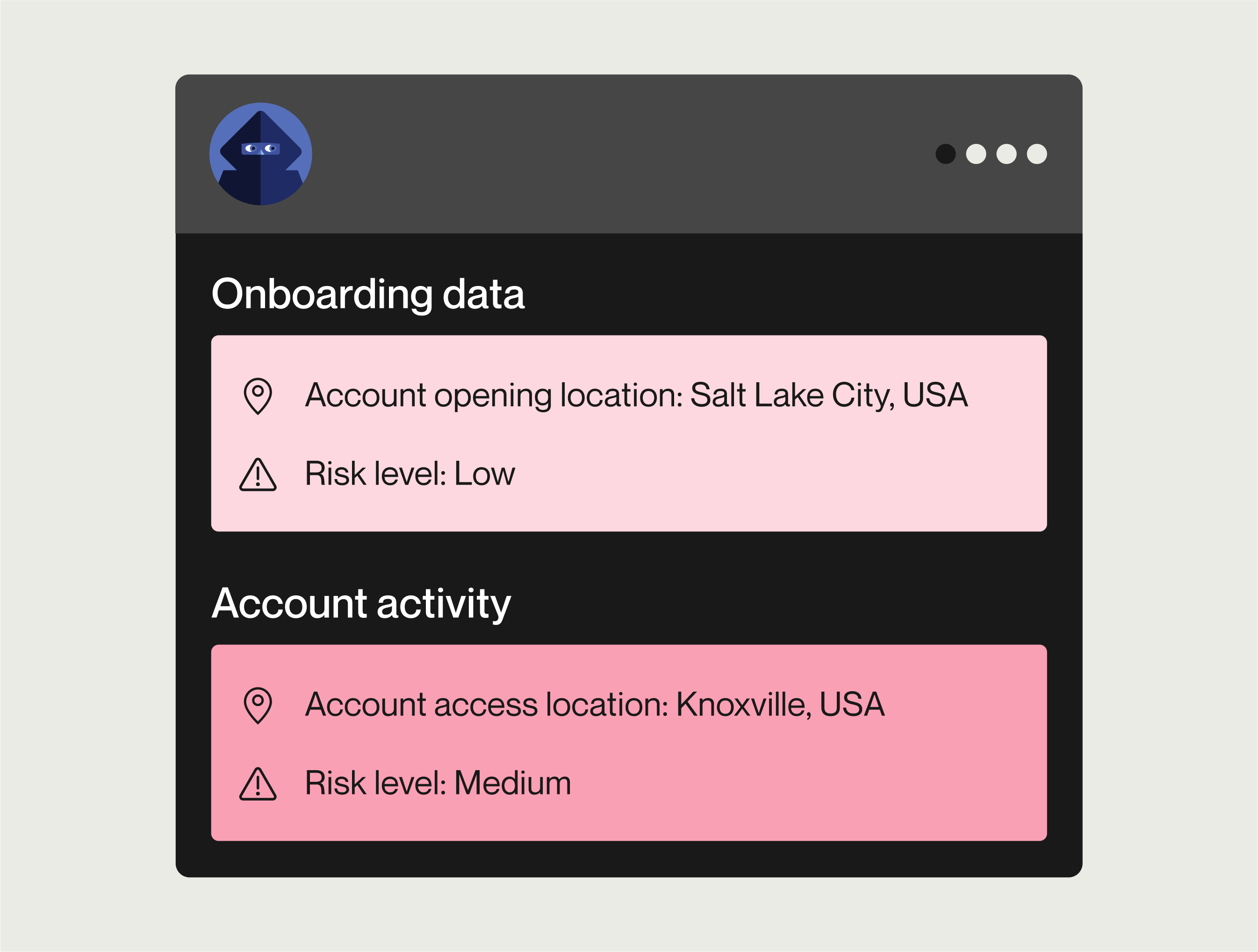

1. Mrs. Smith logs into her mobile banking app from Costa Rica.

To assess the login’s legitimacy, Alloy compares real-time data to historical data or baseline of normal behavior.

When Mrs. Smith first opened her bank account at home in Salt Lake City, Alloy’s initial KYC, AML, and fraud checks assigned her customer profile a “low” risk rating. However, because Mrs. Smith attempted to log in from an unusual location, her bank sent the information through Alloy’s identity and fraud prevention platform for additional due diligence. Because the current customer behavior doesn’t follow known patterns, Mrs. Smith’s customer risk rating is raised to ‘medium.’

2. Mrs. Smith initiates the transfer to the pet sitter.

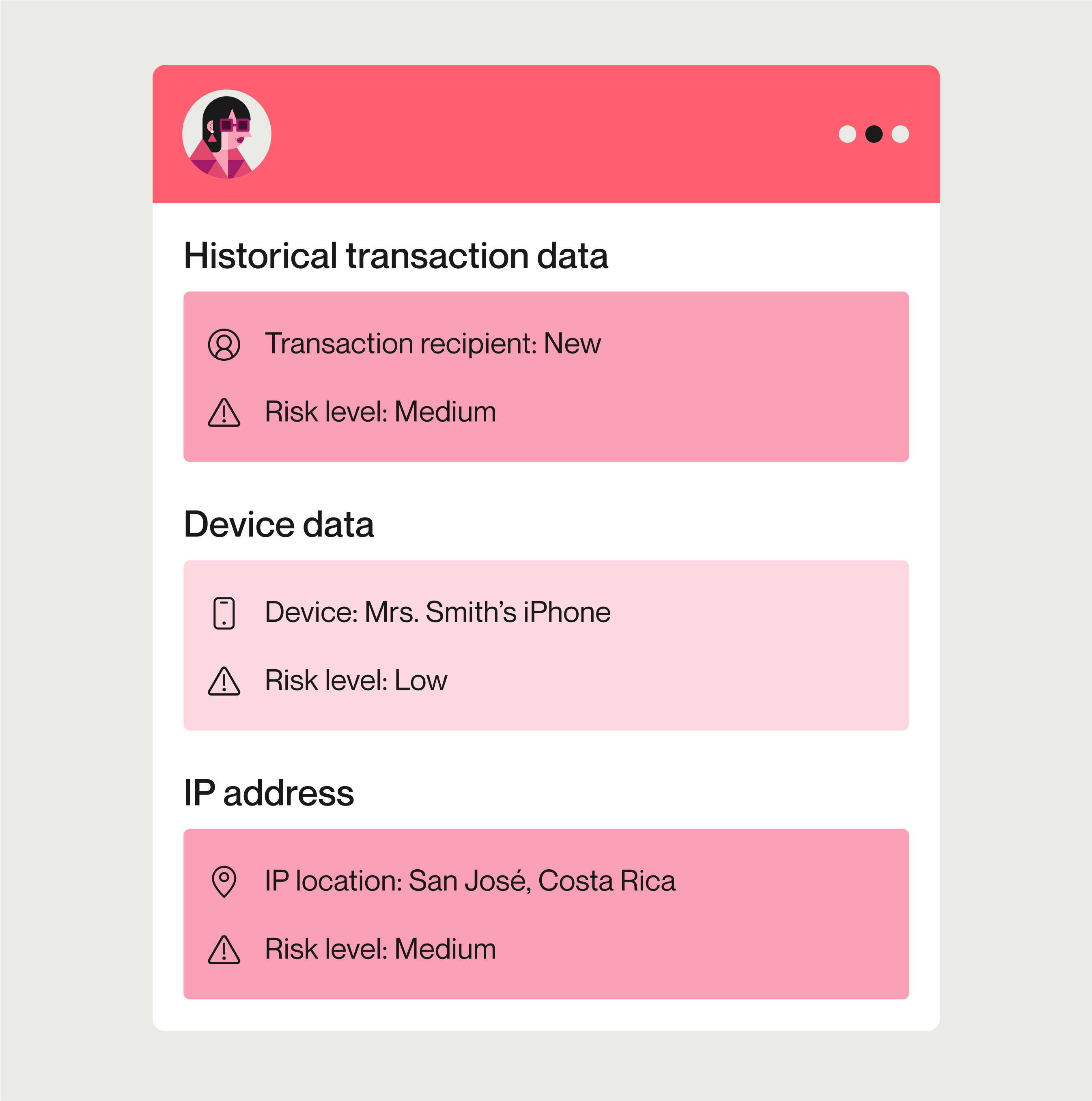

When Mrs. Smith initiates a transfer to her pet sitter, historical data indicates that the recipient is new because the Smith family is accustomed to paying their sitter in cash.

Using customizable workflows that align with the financial institution’s risk tolerance, Alloy issues a call to its third-party data providers, pulling from a combination of device, IP address, and behavioral signals to evaluate the customer’s risk level. This additional due diligence allows the bank to intercept suspicious activity before funds ever leave the account, creating a necessary fraud prevention checkpoint without unnecessary customer experience hurdles.

3. Mrs. Smith completes the transfer to the pet sitter.

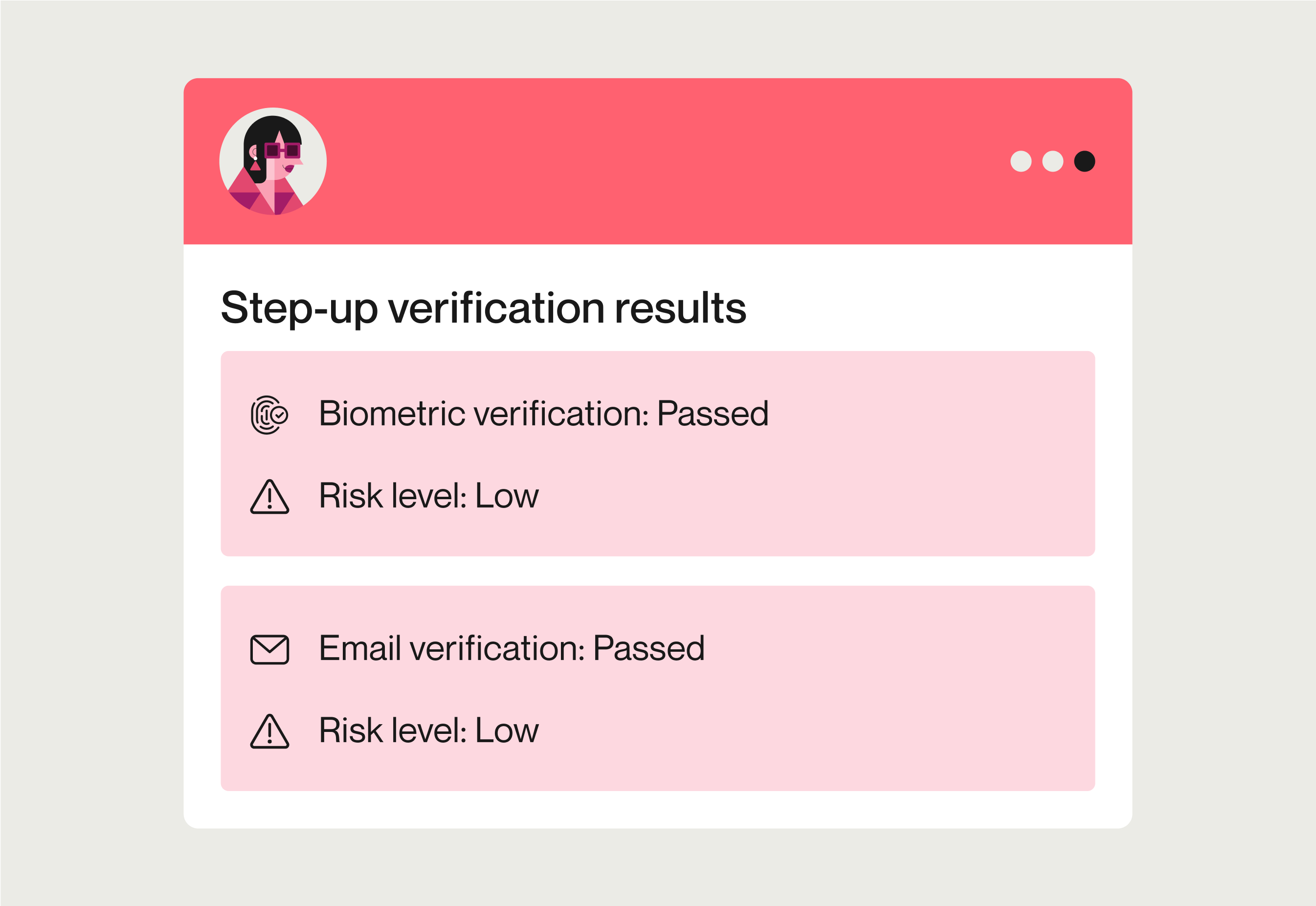

Based on Mrs. Smith’s updated risk rating, her bank needs to perform due diligence to ensure the person initiating the transfer is Mrs. Smith. Alloy triggers an automated step-up verification protocol specific to the risk scenario.

Because of the risky login, Mrs. Smith must confirm her identity by entering the one-time passcode sent to her email on file before she can transfer money. Once she completes this step, Mrs. Smith’s bank requests biometric verification using FaceID, which Mrs. Smith passes without issue.

Instead of freezing the account and forcing Mrs. Smith to place an international call with her bank, Alloy’s adaptive step-up creates a friction-right customer experience. Financial institutions and fintechs can configure different verification methods (like document checks, one-time passcodes, etc.) based on the type of risk detected — ensuring the right balance of security and convenience for each situation.

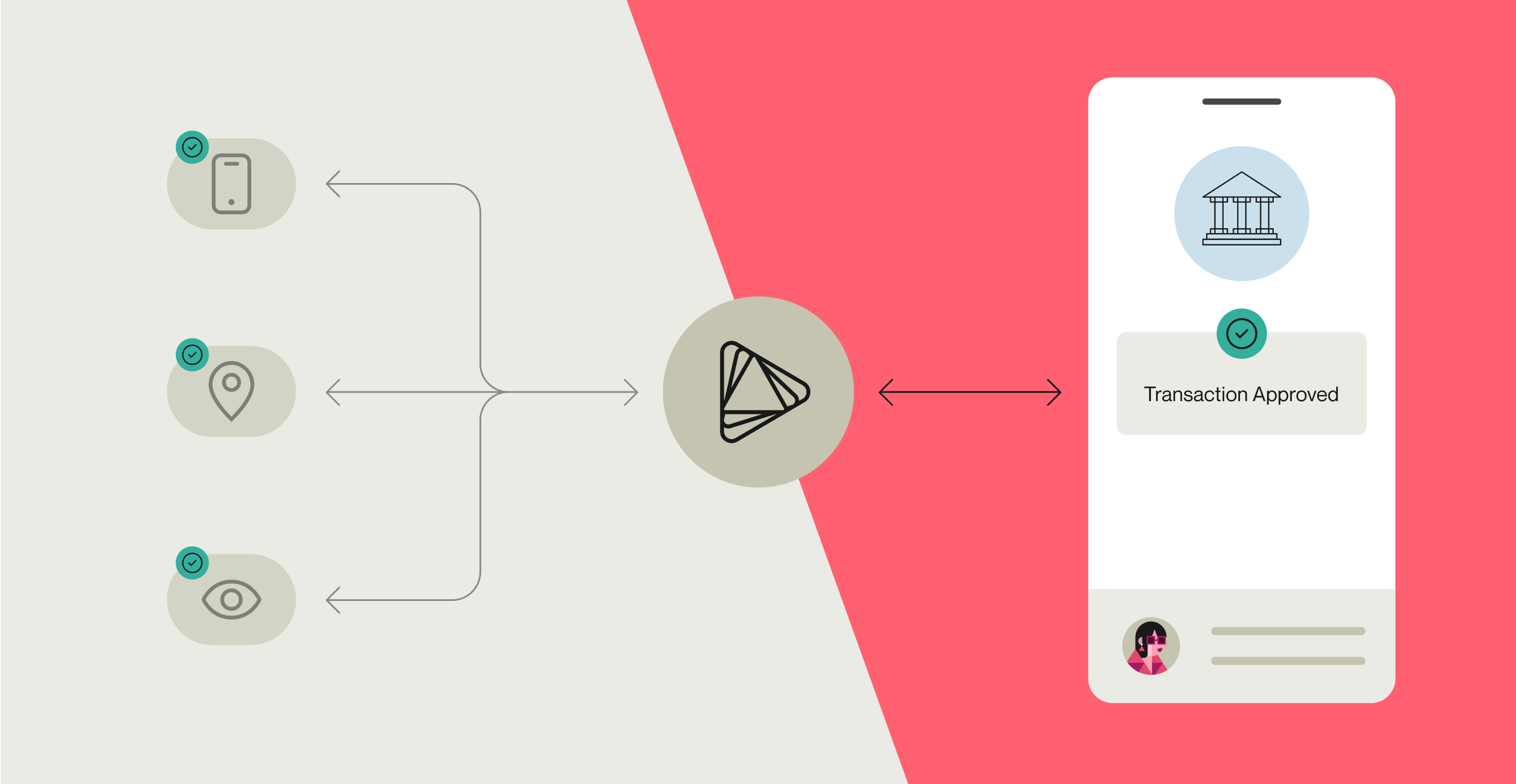

With the identity verification complete in under a minute, Mrs. Smith is able to finalize the transfer. The money arrives in the pet sitter’s bank account, and she brings the family’s dog to the veterinarian for treatment.

Scenario 2: The fraudster

While the customer experience went smoothly for Mrs. Smith, things would shape up differently if her account were taken over by a fraudster. Here’s what this process might look like.

1. A fraudster gains access to Mrs. Smith’s online banking account.

Mrs. Smith’s credentials are stolen in a data breach. A few weeks later, a fraudster uses them to log in to Mrs. Smith’s online banking account.

2. The fraudster attempts to gain control over the account.

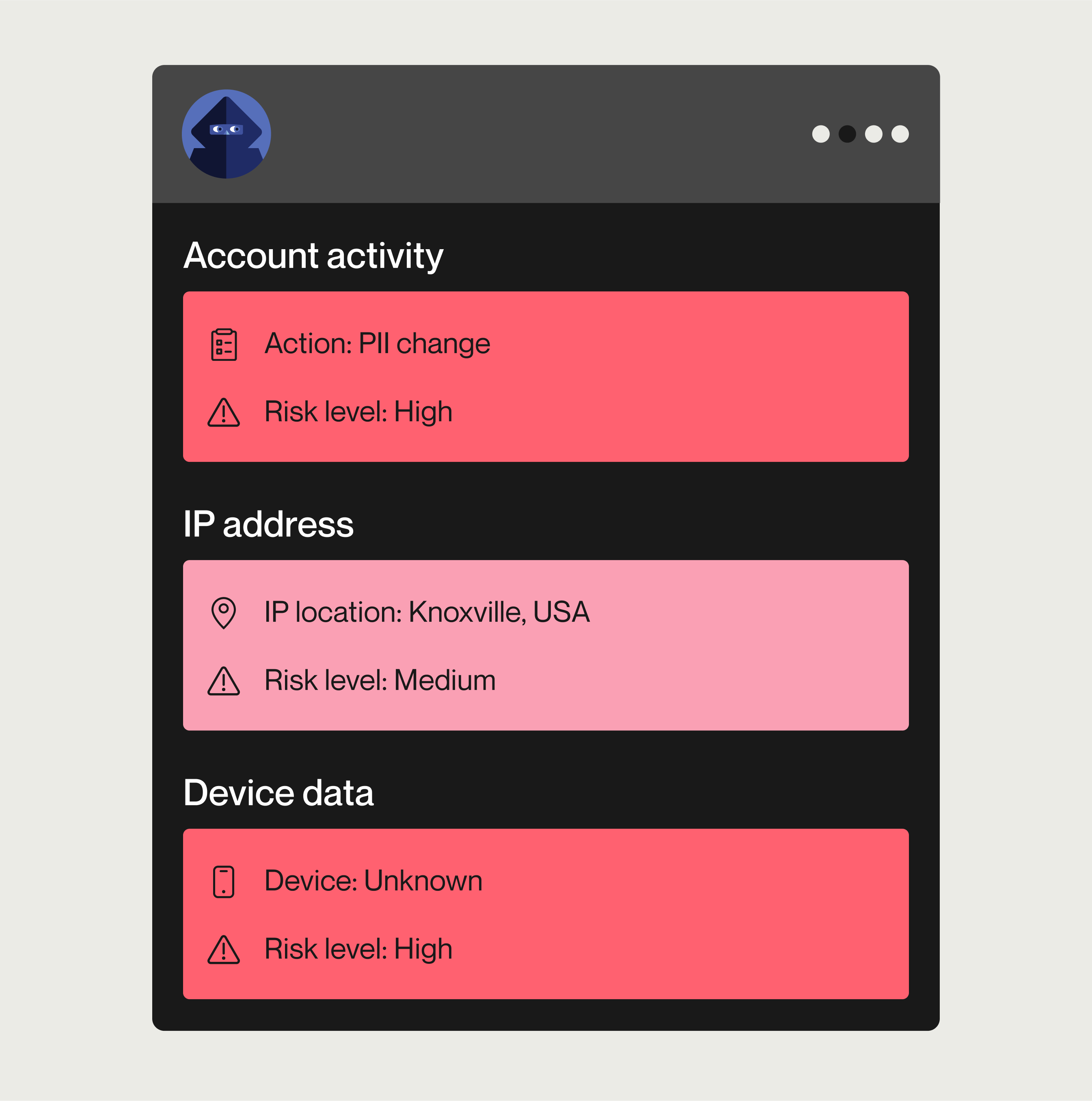

The fraudster attempts to change the contact info associated with the account, switching Mrs. Smith’s email and phone number to ones the fraudster can access. If the fraudster can do this successfully, not only will it lock Mrs. Smith out of the account, it will also prevent Mrs. Smith from receiving alerts and communications from her bank about account activity.

The change request raises red flags with Mrs. Smith’s bank, which runs the customer account through Alloy for additional due diligence.

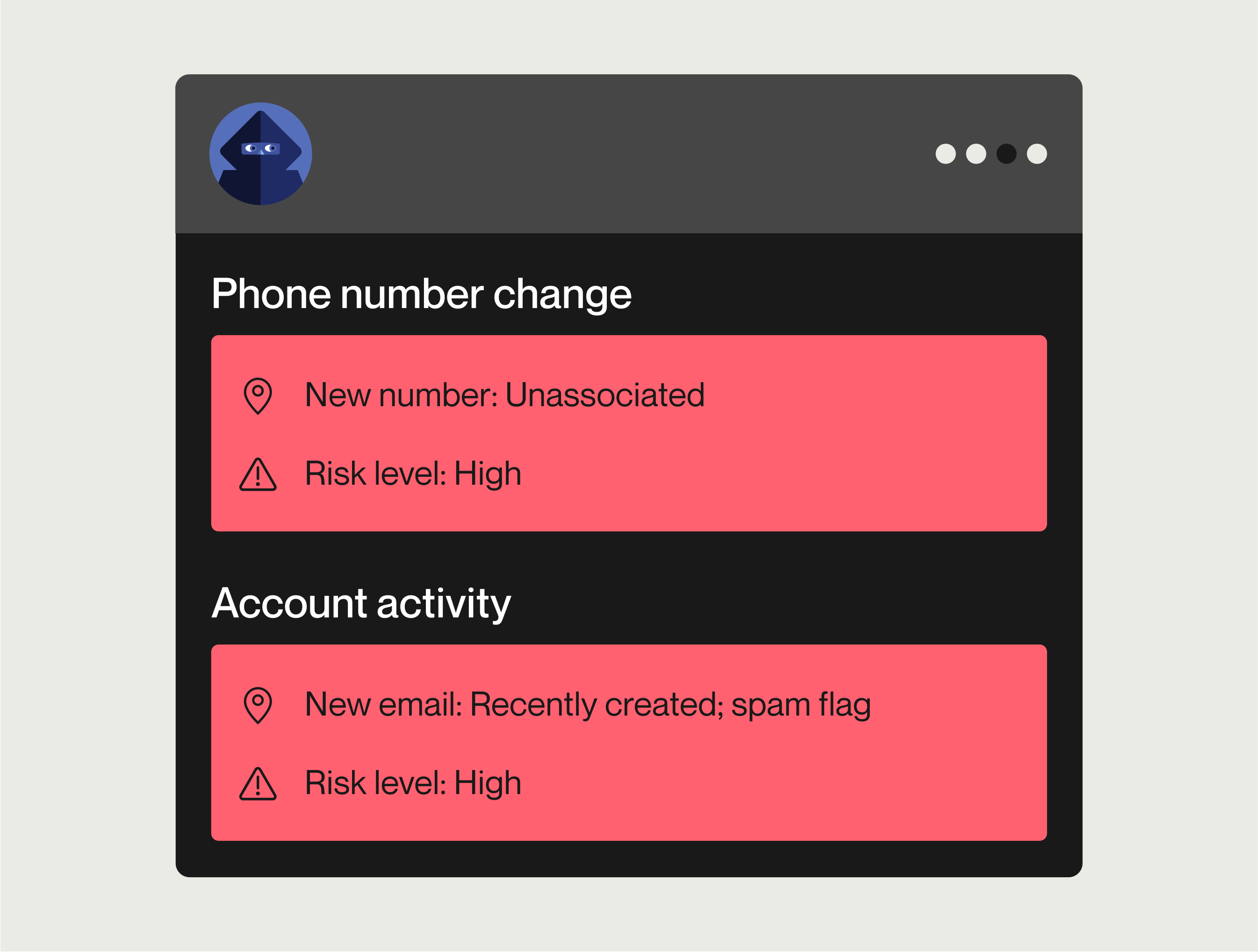

Alloy triggers a call to its data service providers to evaluate identity risk by re-running KYC checks on the new customer information. The data reveals that the new phone number is not associated with Mrs. Smith. Additionally, the email address was recently created and has already been flagged for sending spam.

3. The bank responds to the fraud attack and stops the fraudster from stealing funds.

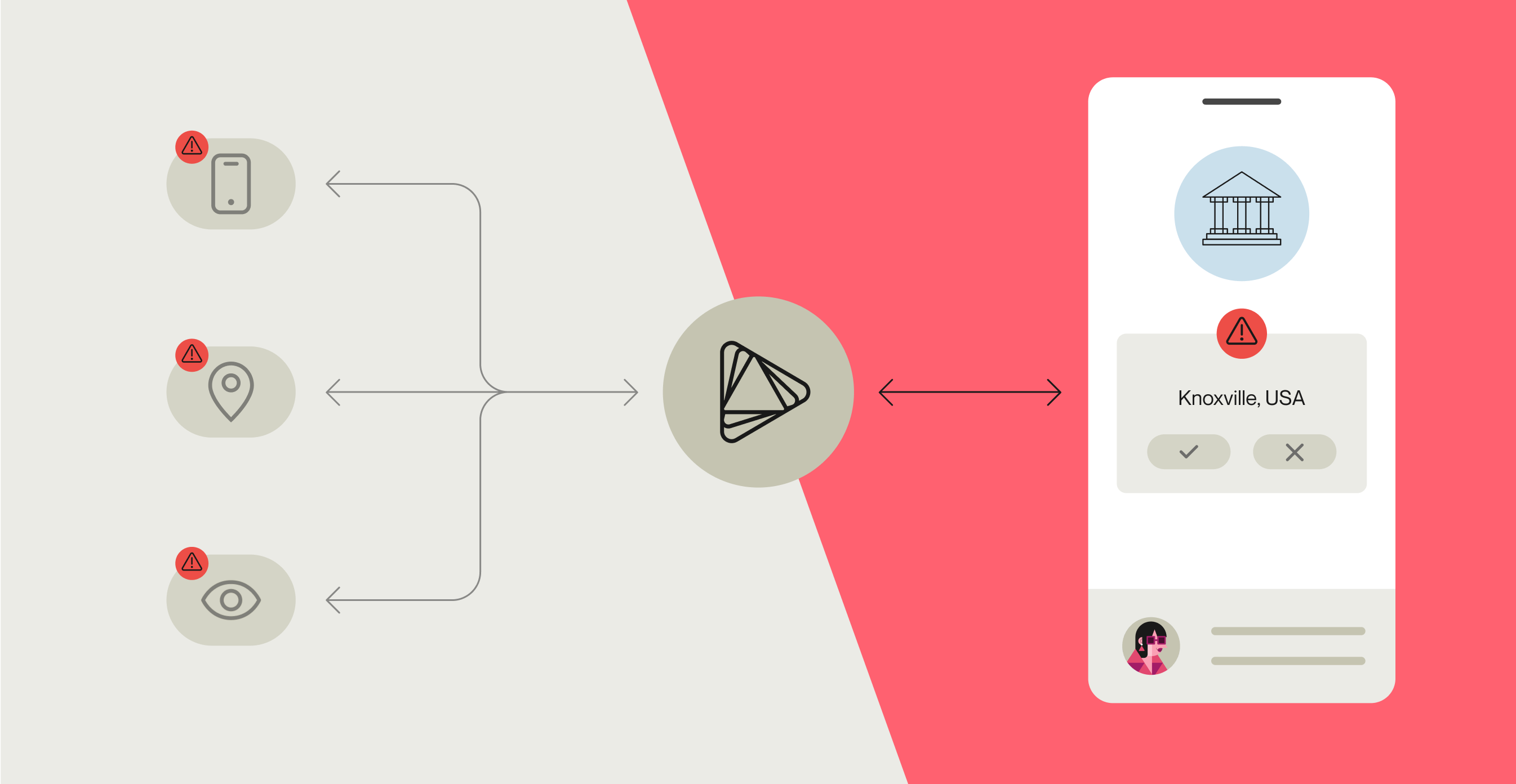

The PII change, coupled with the suspicious device, IP data, and unassociated contact information, increases Mrs. Smith’s customer risk rating. Alloy notifies the bank’s systems to enforce blocks on the login and the PII changes due to the high customer risk level and the unassociated email and phone number.

The bank triggers a fraud investigation and sends an alert through Mrs. Smith's historically verified contact information about the suspicious login attempt. When Mrs. Smith receives this notification, she confirms with her bank that she didn't attempt to log in from Knoxville or request any contact information changes.

Alloy's real-time risk detection successfully prevents financial loss and safeguards Mrs. Smith’s account by intervening at key moments before funds are moved. Because of its ability to pinpoint identity risk and immediately block unauthorized access, Alloy saves the bank significant time and resources — eliminating the complex process of fund recovery.

Alloy offers a single source of truth for fraud prevention teams.

Take every opportunity to detect and prevent fraud throughout the customer lifecycle.

Ready to get started?

Learn more about how you can protect your customers' funds while creating seamless experiences.

KJ McAlpin is a Senior Content Marketing Manager, Fraud Strategy at Alloy, where they specialize in writing about fraud prevention, regulatory compliance, and innovation in financial services. With a focus on helping financial institutions and fintechs navigate an evolving risk landscape, KJ highlights trends shaping the future of identity, fraud, and regulation. Outside of work, they enjoy traveling, journaling, and spending time with their two black cats.