Fighting friendly fraud and chargeback fraud in financial services

Apr 9, 2025

Preventing chargebacks starts with better understanding and identifying friendly fraud

Key Takeaways:

- Financial institutions and merchants lose billions in revenue each year due to friendly fraud, and this problem is accelerating rapidly. According to Datos Insights, global chargeback volume is projected to surge to 337 million annually by 2026 — representing a 42% increase from 2023 figures.

- But efforts to curb chargeback fraud can hurt the customer experience: Roughly one in six cardholders (17%) will slow or stop their card activity after experiencing an unsatisfactory charge dispute process, according to an analysis by Mastercard.

- Advanced data analytics, cross-departmental information sharing, and strategic authentication methods can significantly reduce fraudulent disputes for financial organizations while preserving the customer experience.

It's a familiar situation — a cardholder scans their bank or credit card statement and spots a charge they don't recognize. With a few clicks, they submit a dispute to their bank or credit card issuer. Hours later, while scrolling through text messages, they realize what the mystery charge was: a night out with friends at a new local spot whose merchant descriptor was unfamiliar.

Consumers juggle an average of 3.9 active credit cards and make dozens of transactions weekly across multiple channels. With fraud and digital commerce both on the rise, it’s no wonder cardholders struggle to accurately identify fraud on their accounts.

For financial institutions and fintechs, the dilemma is how to distinguish between genuine disputes, innocent confusion, and intentional friendly or chargeback fraud — all while maintaining customer trust and controlling operational costs that can reach $70 per case.

What is friendly or chargeback fraud?

In financial services, “friendly fraud” and “chargeback fraud” are often used interchangeably. But, there is a difference:

Chargeback fraud describes a broad category of fraud affecting chargebacks

Chargebacks are a federally mandated consumer protection mechanism that allows cardholders to dispute a transaction with their financial service provider. When a cardholder questions a transaction on their credit or debit card statement, their card issuer must investigate. Often, the outcome is a funds reversal to reimburse the customer.

Friendly fraud is when a legitimate customer commits chargeback fraud

Friendly fraud is where a consumer disputes a legitimate transaction with their financial service provider. A type of first-party fraud, friendly fraud gets its namesake from the fact that it’s committed by the actual cardholder instead of an unknown third-party. These “citizen fraudsters” have different beliefs and techniques from traditional fraudsters, necessitating a unique fraud prevention approach.

Learn the difference between first- and third-party fraud

How is friendly fraud committed?

Cardholders who commit friendly fraud may do so knowingly or unknowingly. Here’s what might cause legitimate customers to commit friendly fraud in each situation:

Accidental friendly fraud

A cardholder might accidentally commit friendly fraud for a variety of reasons.

- Statement confusion — The cardholder may not recognize the merchant name on their statement.

- Forgotten purchases — The cardholder may forget making the purchase entirely.

- Family member purchases — A member of the cardholder’s household may make a purchase without informing the cardholder.

- Subscription confusion — The cardholder may have signed up for recurring billing without realizing it.

In many cases, a customer may initiate a chargeback because it’s the easiest way to get their money back after an unsatisfying merchant experience: 72% of cardholders have said that convenience has driven them to file a chargeback claim.

It's not solely buyer dissatisfaction driving fraud; technological advancements, particularly in e-commerce, have introduced new opportunities for unintentional fraud. Shared online services can lead to accidental chargebacks from family member purchases. For instance, a child with access to a shared device could use voice commands to make unauthorized purchases that look a lot like fraud. (“Alexa, get me the PS5 from Amazon.”)

Deliberate friendly fraud

Cardholders may willfully perform illegitimate chargebacks for reasons like:

- Buyer's remorse — The cardholder regrets a purchase and doesn’t want to pay for it.

- Intent to shoplift — The cardholder makes a purchase with the intention of abusing the dispute process to avoid paying.

- Return policy abuse - The cardholder may find it easier to dispute a charge than to adhere to a retailer’s return policy, especially if the policy is unclear or restrictive.

- Service exploitation — The cardholder uses a service (like a hotel stay or a ride share), then disputes the charge to avoid paying.

More than a third (43%) of consumers admitted to committing first-party fraud in a 2024 survey by Socure, including by disputing legitimate charges. Of those who confessed to fraud, 60% of offenders cited financial hardship as the main driver.

How big of a problem is friendly fraud?

It’s estimated that six out of every 1,000 transactions result in a chargeback. Financial institutions must distinguish between legitimate disputes and those originating from fraudulent transactions, often with limited evidence, and while under pressure from regulators to protect consumer rights.

Most chargebacks are a result of third-party fraud, not friendly fraud

Despite so many consumers admitting to committing friendly fraud, Mastercard determined 80% of chargebacks to be the result of fraud committed by unauthorized third-parties in card-not-present (CNP) transactions. These chargebacks are legitimate because they involve unauthorized transactions involving stolen payment credentials — not the real cardholder making purchases and then falsely disputing them. The cardholder is a victim in these cases, properly exercising their rights under consumer protection laws.

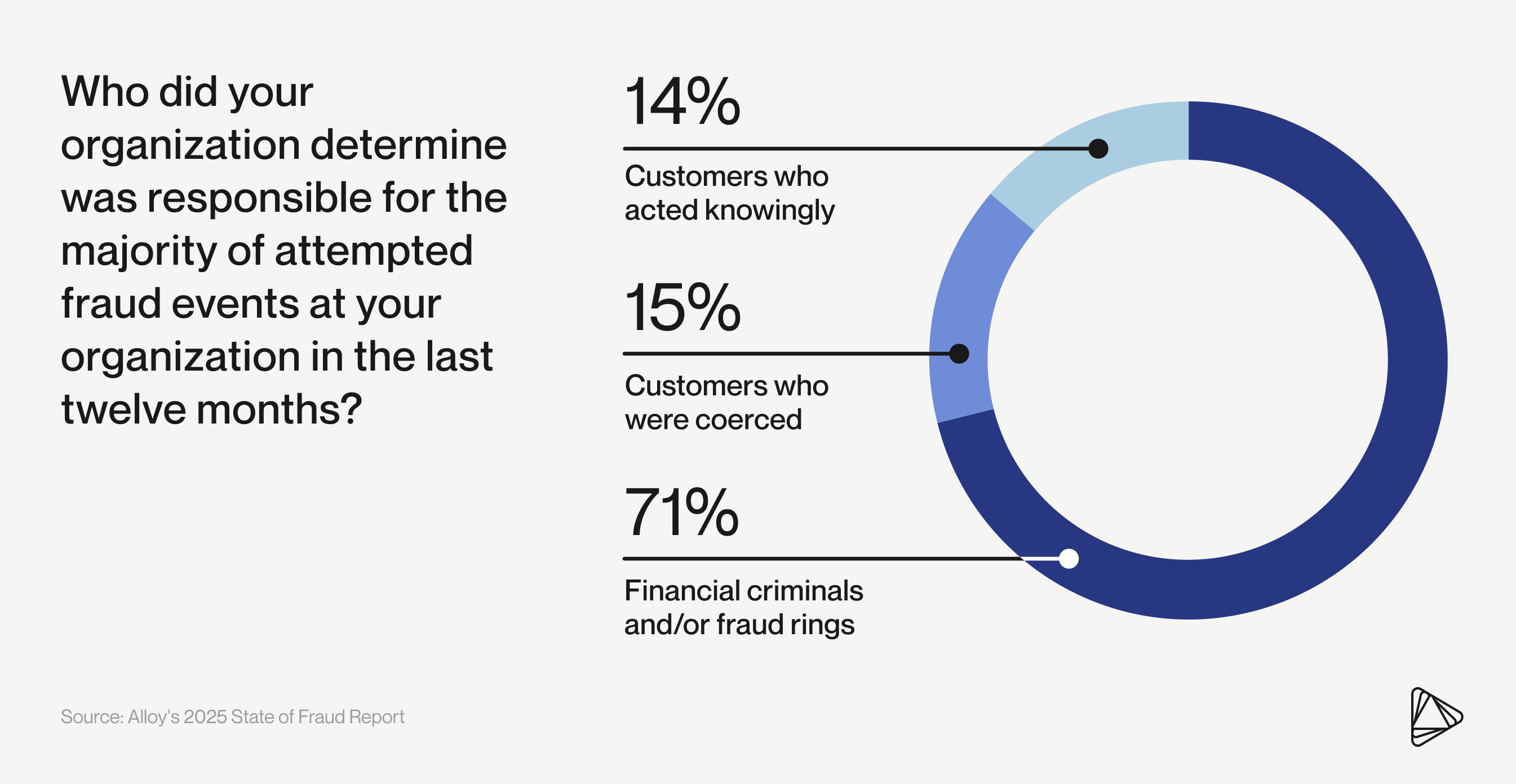

Mastercard’s findings on chargebacks align with broader fraud trends: Last year, 71% of decision-makers determined that financial criminals and fraud rings were the main culprits behind fraud attacks at their financial institution or fintech, according to Alloy's 2025 State of Fraud Benchmark Report.

Short on time? Get our top takeaways from the 2025 Fraud Report.

Who suffers the cost of friendly fraud chargebacks?

Financial service providers, card issuers, and cardholders all share the cost of friendly fraud chargebacks.

Financial institutions and fintechs

Banks, credit card companies, and payment processors bear significant costs from friendly fraud chargebacks. They must dedicate resources to investigating claims, reviewing documentation, and arbitrating disputes between merchants and consumers. These organizations often maintain specialized departments solely for handling chargebacks, representing a substantial operational expense.

When friendly fraud occurs, financial service providers will often get caught in the middle of disputes that are difficult to verify. They may initially cover the disputed amount while an investigation is pending, affecting their cash flow. Additionally, high volumes of chargebacks require sophisticated fraud detection systems and staff training, further increasing operational costs.

The reputation of financial institutions and fintechs can also suffer if they're perceived as having inadequate fraud protection measures or overly complex dispute resolution processes, potentially leading to customer attrition. If the dispute process is unsatisfactory, one in six cardholders (17%) will slow or stop their card activity.

Merchants

Merchants facing friendly fraud chargebacks don’t just lose money from the sale, they also pay a chargeback fee. Depending on the agreement between the merchant and the issuer, the merchant could pay up to $100 for each chargeback, and that doesn’t even cover the expenses the bank or fintech spends on these claims.

Like financial service providers, merchants dedicate significant resources to investigate disputes, and risk losing small business customers as a result of this friction. If the chargeback process gets too frustrating for merchants, they might just go looking for a different payment processor. If merchants have too many chargebacks, some payment processors might penalize them with a higher processing fee or drop them altogether.

Take, for instance, how Chicago restaurants fell prey to this scheme in 2022. Malicious diners enjoyed their meals and then contacted their banks to claim that those charges were unauthorized. These restaurants may not have the manpower to dispute the customers' claims. So, the chargebacks, along with the fine charged by the payment processor, eat into the restaurant’s bottom line.

Cardholders

Finally, cardholders can also face the brunt of chargeback fraud. Legitimate disputes can undergo lengthy, detailed scrutiny, and they might have to wait a long time to get their money back — or not get it back at all.

Moreover, cardholders who frequently file chargebacks, even legitimate ones, may find themselves flagged in fraud monitoring systems. This can lead to declined transactions, account restrictions, or even blacklisting from certain merchants or payment platforms. Some financial institutions may close accounts of customers with excessive chargeback activity, damaging the consumer's banking relationships and credit history.

In cases where friendly fraud is widespread, merchants and financial institutions often implement stricter verification processes, creating additional friction for all consumers during checkout. This results in longer processing times, more identity verification steps, and potentially higher prices as businesses try to offset their chargeback losses. Ultimately, the collective cost of chargeback fraud gets passed on to all consumers through higher prices for goods and services.

Why do financial institutions and fintechs struggle to fight chargebacks?

Effective chargeback management is crucial, but many institutions lack the systems and processes for it. Often, financial institutions and fintechs responding to cardholder disputes are navigating complex operating systems, lacking efficient triage, and dealing with less-than-ideal quality assurance, among other issues.

For instance, there’s a lack of clarity in most banks’ operating models about which team is responsible for customer experience. This lack of coordination causes problems for customers and slows down dispute resolutions and credit processing.

Different departments — like the call center, dispute research team, and back office — do have opportunities for better collaboration. But if they are using disparate systems, they could each be maintaining their own data sets, or even creating different risk profiles of the same customer. As a result, they wind up locked within data silos that impede data sharing and analysis.

The law protects consumers

Although the Fair Credit Billing Act (FCBA) — the law that prevents unfair billing practices in the United States — was intended to protect consumers from unauthorized and fraudulent charges, many individuals misuse this trust and abuse issuers' zero liability policies. Financial institutions and fintechs struggle to figure out precisely what happened in the aftermath of a disputed transaction, only having access to the limited information provided by the individual or business.

According to PYMNTS, "Online statements are less than clear, sometimes without explicit merchant identifiers or other hallmarks that can dispel any ambiguity. Starting and pursuing a dispute has a knock-on effect, as financial institutions…and merchants wind up incurring costs — in terms of time and money — to investigate the dispute."

However, some card regulations that prioritize consumer protection also provide guidance that can help financial institutions and fintechs navigate the dispute process:

- Regulation E, which implements the Electronic Fund Transfer Act (EFTA), outlines the consumer's responsibilities for reporting any unauthorized electronic funds transfers (EFTs).

- Regulation Z, which implements the Truth in Lending Act (TILA), requires lenders to resolve disputes in a timely manner, provide monthly billing statements to borrowers, and proactively notify borrowers any time their lending terms change.

When claims teams are more prepared to address disputes, they are also more prepared to spot outliers in consumer behavior. These guidelines help financial institutions and fintechs to:

- Set consumer expectations

- Handle disputes with more consistency

- Set a baseline for how disputes should be resolved

- Potentially identify more indicators of chargeback fraud in the process

Existing fraud prevention models are flawed

Most fraud models are broken. When financial institutions and fintechs only examine fraud at the transaction level, it puts them in a reactive position rather than proactively identifying and stopping chargeback fraud. In the long run, this approach can result in losing merchant trust, credibility, and funds. Instead, they should focus on getting to know the person behind the transaction:

- Is the person's identity authentic?

- Are they using someone else's account?

- Have they committed or are they planning to commit fraud?

- Historically, have they filed a large number of credit disputes?

Overall, this deeply flawed dispute cycle contributes to the rise in chargeback fraud nationwide.

Why identity should be at the center of your fraud prevention strategies

How can financial institutions and fintechs defend themselves against chargeback fraud?

To improve their chargeback fraud prevention, some financial institutions and fintechs are adopting claims abuse procedures to keep track of the number of disputes filed for each customer. But they still get easily overwhelmed by the volume of disputes.

Again, the challenge of data silos comes up. When teams work in separate systems, they fail to see the complete customer profile. For instance, if a customer were to dispute a mere $150, the claims team handling the dispute might not notice that the fraud team also put a hold on a recent deposit due to suspicious activity. Likewise, if a customer filed a large number of disputes, and that information is tracked in the dispute claim system, fraud teams might not have access to those records.

This happens at financial institutions and fintechs every day. The onboarding workflow determines that a customer is low risk, while an ongoing monitoring workflow later picks up on suspicious behavior. When data insights are not shared, it gets in the way of catching chargeback fraud. When claims and fraud teams have better context and access to customer data, they set better standards of normal customer behavior and spot red flags much faster.

The solution? Continuous and rigorous monitoring throughout the customer lifecycle

For financial institutions and fintechs struggling to prevent friendly or chargeback fraud, modern identity and fraud prevention platforms provide essential visibility into customer behavior, including the ability to prevent more types of chargeback by proactively identifying high-risk customers.

Alloy’s identity and fraud prevention platform uses machine learning to create dynamic customer profiles that evolve throughout the customer journey. Our fraud detection tools conduct ongoing behavioral and account monitoring, performing real-time interventions — such as step-up verification or automated interdiction — against common types of fraud, including fraudulent chargebacks.

Platforms like Alloy offer a foundation for improving chargeback rates by stopping suspicious card transactions ahead of time. Not only do these platforms address verification needs by bringing multiple data sources (including real-time transaction data) together under a unified platform for fraud and identity risk — they also prevent the time-consuming customer disputes that can chip away at profitability.

Despite the proliferation of financial losses related to fraudulent activity, like account takeover attacks and credit card chargebacks, deterrents like integration challenges can stand in the way between financial organizations and new forms of chargeback protection. Alloy's fraud prevention tools eliminate the need for disruptive "rip and replace" implementations or major system overhauls. Instead, it seamlessly connects with existing infrastructure while leveraging multiple third-party solutions — from traditional personally identifiable information (PII) to card payment data — to build a more complete and accurate customer profile. Beyond the technology, Alloy's expert team provides valuable support in analyzing fraud patterns and continuously refining your prevention processes.

Don't let friendly fraud win. See how Alloy can help fight chargebacks.

Learn how our platform can meet your financial organization’s unique needs. Contact us to request a demo or learn more about our platform.

KJ McAlpin is a Senior Content Marketing Manager, Fraud Strategy at Alloy, where they specialize in writing about fraud prevention, regulatory compliance, and innovation in financial services. With a focus on helping financial institutions and fintechs navigate an evolving risk landscape, KJ highlights trends shaping the future of identity, fraud, and regulation. Outside of work, they enjoy traveling, journaling, and spending time with their two black cats.