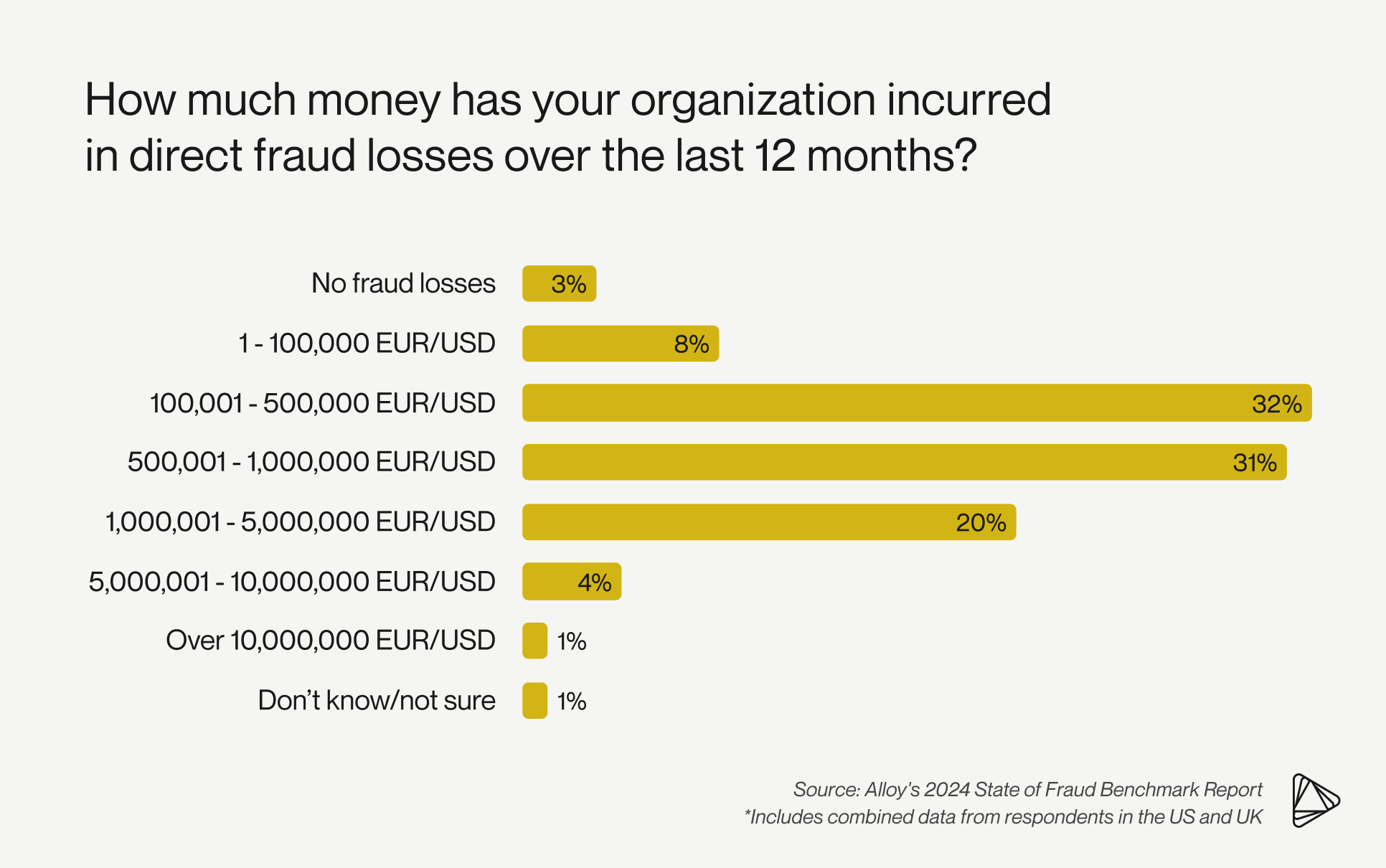

NEW YORK, January 25, 2024 -- Alloy, the identity risk management company behind over 500 leading banks and fintech companies, today released its 2024 State of Fraud Benchmark Report, finding that after years of steadily increasing fraud rates, the number of reported fraud attacks have begun to even out – and for some organizations, to decelerate. Despite that progress, fraud has still resulted in significant financial losses: 56% of respondents lost more than 500,000 (EUR/USD) to fraud in the last 12 months, and 25% lost over 1M (EUR/USD) in that time.

Alloy’s State of Fraud Benchmark Report tracks shifting trends in financial fraud, based on a survey of over 450 fraud decision-makers working at banks, credit unions, and fintechs in the US and UK. The report offers an inside look at how companies prepare for, experience and respond to fraud, and how that fraud translates to direct financial losses.

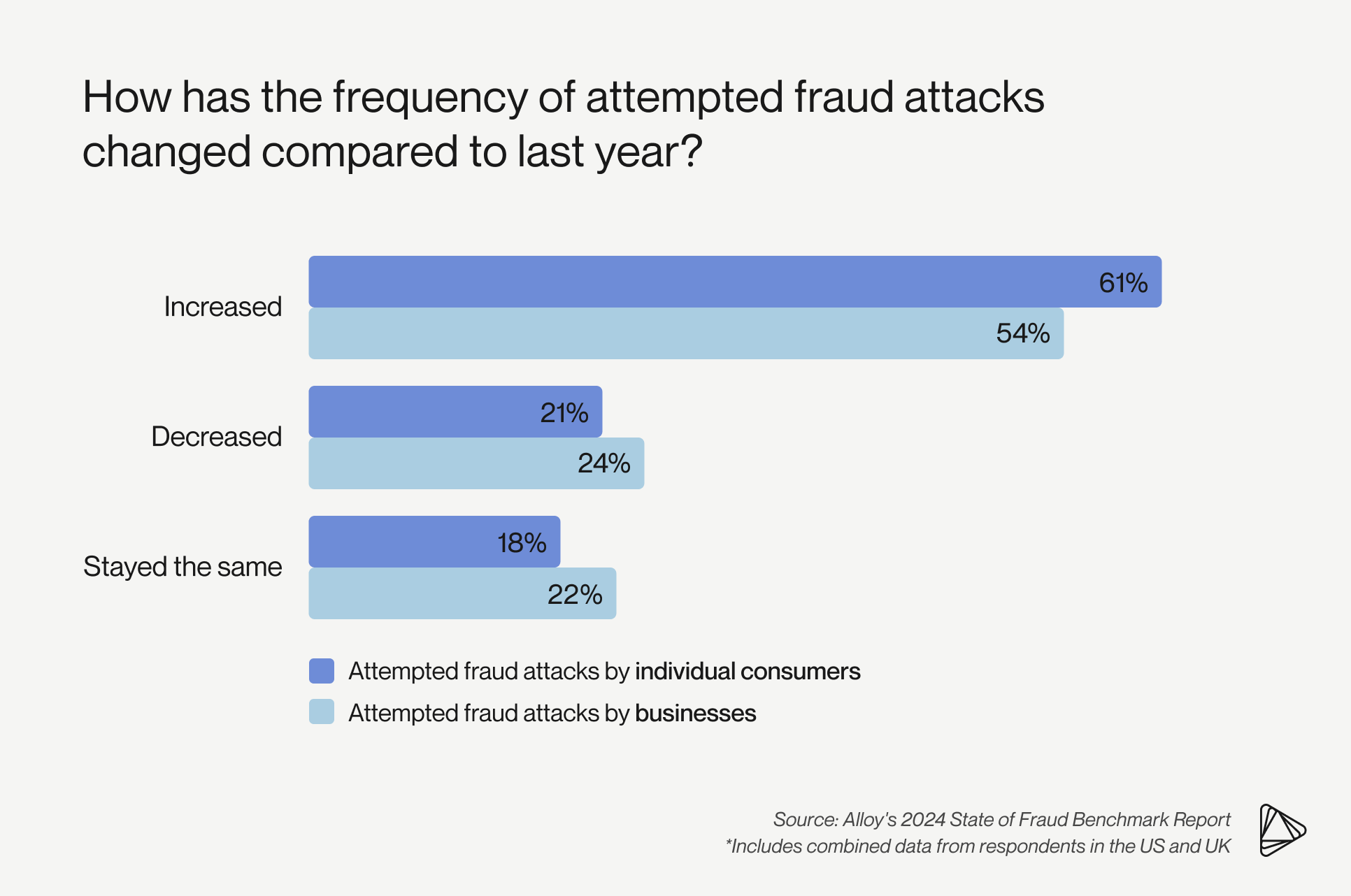

This year’s report revealed a drop in the number of companies that have experienced 1,000 or more fraud attempts over the past year: In 2023, 35% of companies experienced 1,000+ fraud attempts, down from 47% in 2022. But it’s not all good news: 61% of companies saw an increase in attempted fraud attacks committed through consumer accounts in the past year, and 54% saw an increase in attempted fraud attacks committed through business accounts.

“It’s encouraging to see companies getting fraud volume under control using the wide array of identity data and technology available on the market,” said Tommy Nicholas, CEO and co-founder at Alloy. “But fraud remains a critical problem because bad actors are always finding new tools—such as generative AI—to steal increasingly large amounts of money.”

On the bright side, business sectors investing in the implementation of new fraud tools were more likely to see decreased fraud attempts last year. 24% of enterprise fintechs and 43% of mid-market banks said fraud attacks by consumer and business accounts decreased at their organizations in 2023. At the same time, 37% of enterprise fintechs and 60% of mid-market banks said they were investing in the implementation of new fraud tools, suggesting that their use of outside technologies may be helping to diminish their fraud volumes. In 2024, more companies are poised to continue their investments in fraud prevention solutions: 75% of companies across all sectors said they plan to invest in an identity risk solution in the next year.

Though identity solutions are helping companies make progress in the fight against fraud, certain types of financial crime continue to plague companies. Businesses across the US and the UK ranked authorized push-payment (APP) fraud as their top fraud driver last year by case volume and losses. Looking ahead, US/UK companies ranked AI-driven fraud (24%) as the type of fraud they are most concerned about in 2024. With both APP fraud and AI-driven fraud frequently resulting from scams targeted at individual consumers, many US/UK companies (53%) also plan to invest in anti-scam education tools over the next year.

Alloy’s report was fielded in November 2023 and includes respondents from growth fintechs (1-100 employees), strategic fintechs (101-500 employees), mid-market fintechs (501-100 employees), enterprise fintechs (1000+ employees), regional banks (<$10M AUM), mid-market banks ($10B - $50B AUM), enterprise banks (>$50B AUM), credit unions/community banks, and online/pure play lending institutions. The report was conducted on behalf of Alloy by Qualtrics, a leading survey platform that powers more than one billion surveys every year.

For more insights, read the full report here.

About Alloy

Alloy solves the identity risk problem for companies that offer financial products. Today, over 500 banks and fintechs turn to Alloy’s end-to-end identity risk management platform to take control of fraud, credit, and compliance risks, and grow with confidence. Founded in 2015, Alloy is powering the delivery of great financial products to more customers around the world. Learn more at alloy.com.