2025 State of Scams Report

Scams are on the rise, and so is confusion over who is responsible

Key takeaways:

- Two-thirds of consumers (67%) believe their financial institutions should reimburse them for money lost in a scam even when they personally authorized the transaction.

- At the same time, more Americans say they are responsible for protecting themselves from scams (39%) than their financial institutions (36%).

- 85% of Americans worry that scams are becoming harder to detect because of AI technologies.

- Younger generations report the highest and most frequent losses. Nearly one in four (23%) Gen Z and Millennial scam victims lost $5,000 or more — a hit 3x bigger than the average cost of rent.

- Fraud prevention and security are non-negotiable for consumers, with 97% saying they are the most important factors when choosing where to bank.

- Yet, nearly seven in ten consumers (69%) expect new account sign-up to take less than 10 minutes, and six in ten (59%) say they experience frustrations opening financial accounts online.

Introduction

Scams have become a defining challenge for modern banking. 73% of Americans have experienced some form of online scam, and the Federal Trade Commission (FTC) logged 2.6 million fraud reports in 2024 alone.

What makes this moment unprecedented isn’t just scale, but speed. AI-powered scams are evolving faster than consumers or financial institutions can adapt to on their own. Consumers and financial organizations are defending against the same threats in real time, creating a rare moment of mutual vulnerability and dependence.

Drawing on a national survey conducted by The Harris Poll, this report surfaces how consumers assign responsibility for scam protection, the expectations they place on their financial institutions, and how advancing technologies like AI are reshaping their trust.

About the research

This report is based on an online survey of 2,000 U.S. adults (ages 21–75) conducted by The Harris Poll from July 8 to July 26, 2025, on behalf of Alloy.

AI-driven scams are testing consumer trust

85% of Americans worry that scams are becoming harder to detect because of AI technologies. Top concerns include impersonations of their bank (28%), voice cloning over the phone (21%), and synthetic identity fraud (18%).

As AI makes it easier to fabricate more convincing communications, phishing stands out as the most common scam experienced by consumers firsthand or by someone they know. Other widespread scams include identity theft, payment scams, credit card fraud, and account takeover attacks.

Alloy insight: These numbers likely understate the true prevalence of scams. Many incidents — such as identity theft — can go undetected for long periods of time, meaning more people may be exposed than survey responses suggest.

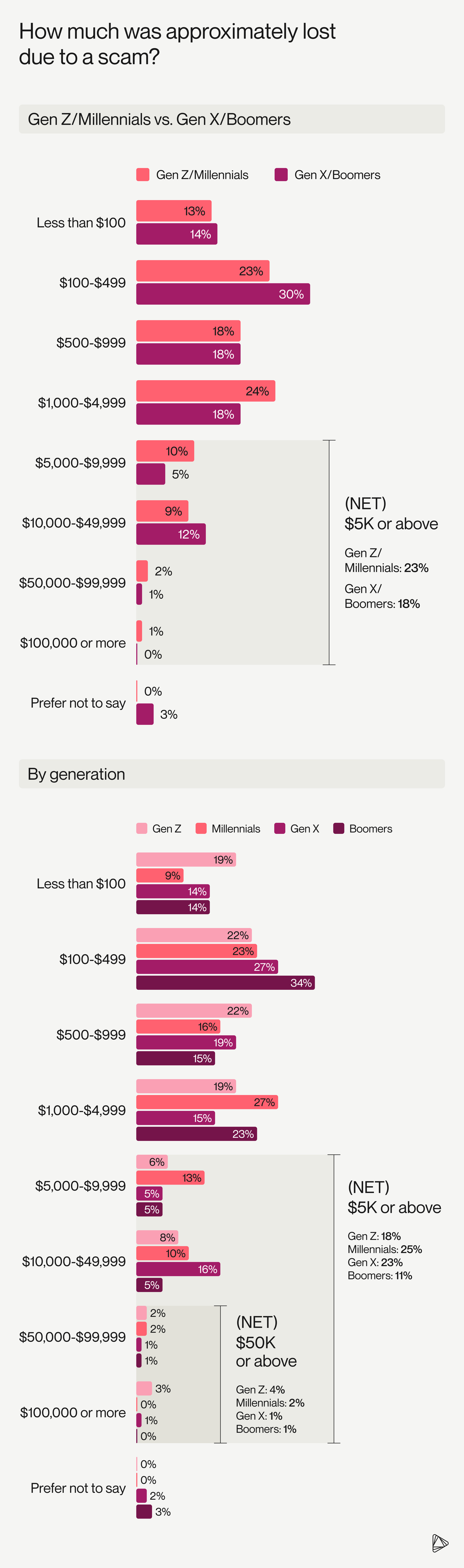

Young people report the highest financial impact

One in five customers who experienced a scam (21%) reported losing $5,000 or more. As a combined category, 23% of Gen Z and Millennial scam victims report losses at this level — more than Gen X/Boomers (18%). This number is especially high for millennials, with one in four (25%) reporting losses of $5,000 or more. Meanwhile, Gen Z reported the highest percentage of losses above $50,000, at 5%.

It’s worth noting that Alloy’s research surveyed adults ages 21–75, so it does not include the Silent Generation (80+). This helps explain why our findings highlight significant losses among younger generations, while FTC data shows the steepest losses among the oldest Americans. Taken together, the two perspectives underscore that scam risk is spread across generations: younger consumers are frequently targeted and often incur major financial hits, while older adults remain especially vulnerable to severe median losses. Younger consumers may also be less likely to report scams to government agencies, instead choosing to handle the fallout directly with their financial institutions and payment app providers.

The emotional consequences of scams outweigh financial ones

The most painful part of a scam isn’t always the money lost. Nearly one in three consumers (29%) cite emotional distress as the worst consequence, outranking financial loss (28%).

Scams also carry social stigma. Many people believe they can spot fraud, so when they don’t, the blow to pride and self-image can be severe: three in four Americans (74%) say falling for a scam feels more embarrassing than making a poor financial choice.

During and after a scam, consumers report feelings of anger, anxiety, and confusion as they try to make sense of what happened and determine how to respond.

Those emotions trigger action: Nearly all Americans (96%) take steps after being targeted by a scam — most often by reporting the event to their FI (63%), placing a credit freeze (52%), or warning friends and family (44%).

Consumers expect financial institutions to provide scam protection

Consumers feel a strong sense of personal responsibility when a scam occurs, but they believe financial institutions share nearly equal responsibility in preventing attacks. At 40%, Gen Z/ Z/Millennials are even more likely to view their FI as being responsible for scam prevention, compared to 32% of Gen X/Boomers.

Fraud prevention and security are non-negotiable for consumers, with 97% saying they are the most important factor when choosing where to bank.

Educational resources remain a valued tool for helping people recognize scams, while advanced safeguards such as AI-driven fraud prevention are also viewed as critical complements. 69% of consumers say they would be willing to trade some privacy for stronger AI protections, and 66% report they would be more likely to choose a financial organization that applies them.

Consumers see their bank as a partner to help them navigate scams

Even after being targeted by a scam, most consumers remain with their bank. Yet loyalty is conditional for some, with 17% of scam victims reporting switching institutions.

When a scam occurs, consumers expect immediate and visible intervention, including freezing compromised accounts (68%), reimbursing stolen funds (67%), and providing continuous updates throughout the process (67%). 87% of consumers say they would lose trust in their bank if it failed to notify them immediately of a scam attempt.

Alloy insight: While banks can freeze or delay activity in cases of suspected fraud or money laundering, they can’t always block an authorized payment, even if it turns out to be a scam. Under the Uniform Commercial Code (UCC §4-401), banks must honor transactions that are “properly payable” — meaning authorized by the customer — or risk liability for wrongful dishonor. This gap between what consumers expect and what banks are legally able to do helps explain much of the frustration around scam recovery.

Beyond freezing accounts, scam victims also expect to have their money returned to them. Consumers view financial institutions as the primary party responsible for recouping losses, with Gen Z/Millennials standing out as the most likely to agree.

Overall, two-thirds (67%) of consumers agree they should be reimbursed even when they personally authorized the transaction.

Expectations rise steadily with age groups — from 56% of Boomers to 66% of Gen X to 70% of Millennials and 77% of Gen Z. This generational progression highlights how younger consumers, in particular, see reimbursement as a core part of their bank’s responsibility in scam recovery.

But the reality often falls short. Of those who sought reimbursement, nearly half (44%) received only a partial refund or nothing at all.

Consumers want seamless financial experiences

The same consumers who demand bulletproof fraud protection also expect to be able to transact and open new accounts easily.

Nearly seven in ten (69%) believe opening an account should take under 10 minutes — yet most aren't getting that experience.

Six in ten Americans (59%) report frustrations during account opening, primarily that the process takes too long (22%) or requires too much information (16%).

Consumers see both safety and simplicity as non-negotiable. Add more security checks, and they might abandon the process. Speed up onboarding, and fraud risk climbs. Institutions are left trying to deliver two outcomes that feel, at times, at odds.

But consumers are willing to compromise if it leads to better scam prevention. 87% say they would spend an extra five minutes setting up security measures for their account, and 82% say they would customize their protections by completing a short questionnaire. While consumers expect financial institutions to be the safety net, they are also prepared to do their part when protections feel purposeful and effective.

Which protections feel most effective depends on who you ask. Younger consumers trust facial recognition and biometric scans. Older consumers want to answer personal questions they've used for decades. This split creates another contradiction for banks: the same security measure that makes younger customers feel protected might frustrate older ones, and vice versa.

The challenge for financial institutions is establishing defense systems smart enough to offer the right level of protection at the right moment. For consumers, it’s finding a financial organization that offers protections that feel reliable, not intrusive.

Conclusion

Scams go deeper than financial loss. The embarrassment of being fooled, the anxiety about whether it will happen again, and the anger at systems that failed to offer protection often drive what consumers do next.

Right now, financial institutions face customers who want contradictory things: speed and security, personal control and institutional protection, minimal friction and maximum safeguards. Gen Z and Millennials, having suffered the steepest losses, are the loudest voices in this chorus. They're rewriting the rules — expecting reimbursement even for authorized payments, trusting biometric authentication over passwords, and insisting on convenience alongside safety.

These contradictions will continue to intensify as AI makes scams more convincing and consumers grow more impatient with digital friction. Banks that treat these opposing demands as an either-or proposition will lose to those that find ways to deliver both.

The path forward involves recognizing that consumers and financial institutions are navigating the same problems, where yesterday's best practices might not work tomorrow. Financial organizations that build lasting trust will be those that adapt as quickly as the threats themselves, going beyond compliance minimums to meet customers where their expectations actually are, not where banks wish they were.

About Alloy

Alloy enables financial organizations to meet evolving consumer expectations around fraud prevention and identity verification. Our platform helps banks, fintechs, and credit unions deliver the seamless experiences customers demand while maintaining the robust protections they expect.